Learn How to Read Your Pay Stub

This is the Day 4 challenge in the #Money30, a month-long bootcamp for personal finance novices. You can read more about the challenge here, and follow along with us on Twitter, Instagram, or email us at feedback@moneymail.com.

TIME BUDGET: 15 MINUTES

If you get a paycheck, you know that a decent amount of your salary doesn't end up in your bank account—it's diverted to things like Social Security, the federal government, and (hopefully) into your 401(k). But if you, like many people, avoid the pain of looking at your pay stub closely each pay period, you may be missing out on a few things.

By breaking down what's on your pay stub, not only will you see where your money is going (a $50,000 salary doesn't actually mean $50,000 in your bank account, after all), but you'll also learn about your pre-tax savings—which will hopefully encourage you to take advantage of all the ways you can lower your tax bill. Here's the breakdown:

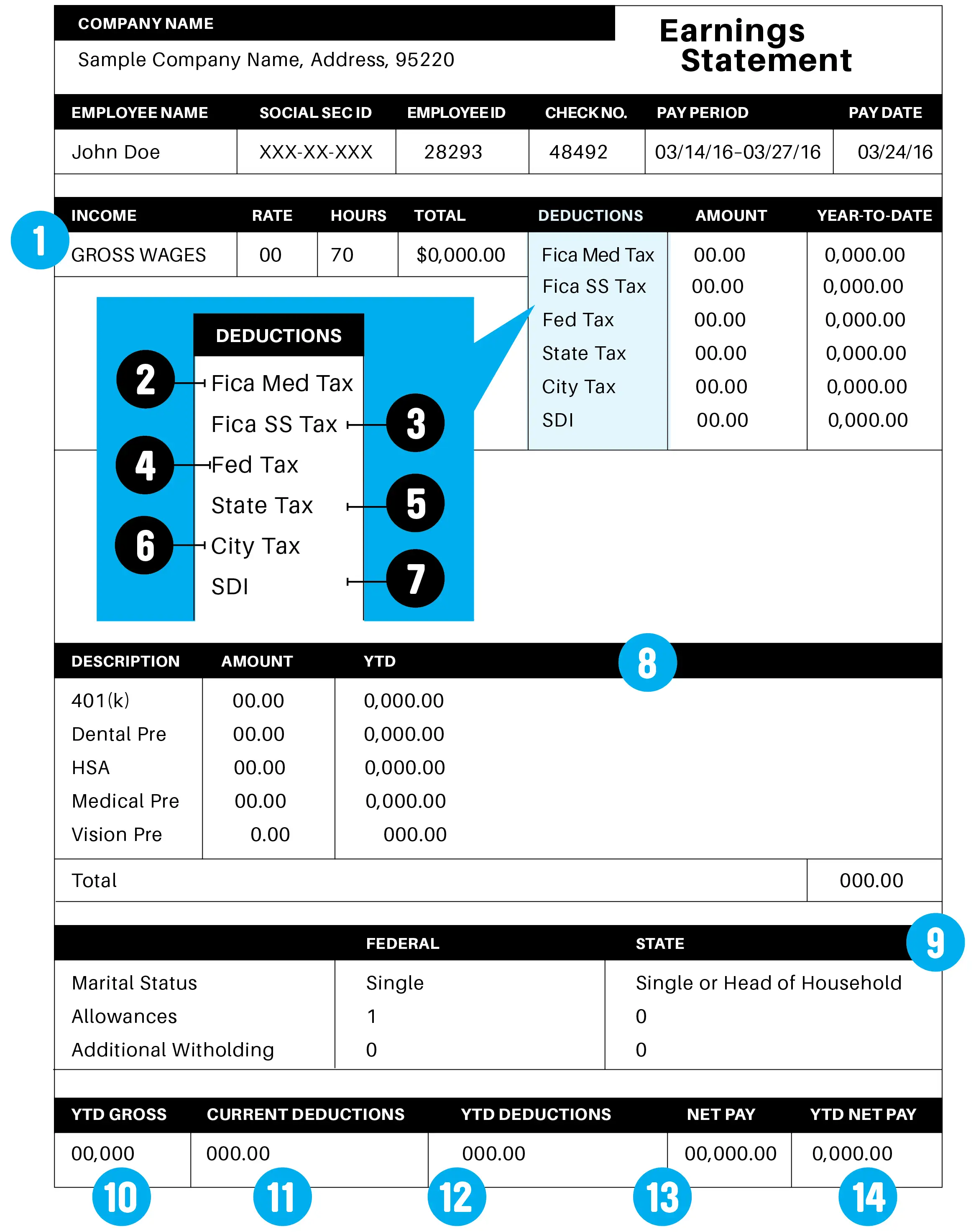

1. Gross Wages

If you are a salaried employee, this is the amount you earn per pay period (your salary divided by the number of paychecks you receive per year). Hourly workers will see the "rate" (pay per hour) and the number of hours worked. If you're eligible for overtime, that will be tabulated too.

For salaried workers, your hours are likely listed as 35 or 70, depending on whether you receive checks weekly or every other week. That's because a lunch hour is automatically deducted from each work day. Just another reason to make sure you don't eat lunch at your desk.

2. Fica Med Tax

“Who’s FICA? Why is he getting all my money?” Perhaps one of the most relatable scenes from Friends is when Rachel receives her very first paycheck at Central Perk, only to discover she isn't making quite as much as she expected. You, too, may be wondering what all of these taxes are that you're paying. FICA, the Federal Insurance Contributions Act, is comprised of Medicare and Social Security. They may be listed together or separately. Medicare taxes are used to subsidize health insurance for people 65 and older, as well those with disabilities and other groups.

3. Fica SS Tax

Social Security, as you may know, is a government program that all working Americans pay into, and which provides income to eligible beneficiaries, typically retirees and those with disabilities. Contrary to what certain politicians say, the program is not likely to run out of money before you become eligible to receive benefits. For millennials, the full retirement age—i.e., the age when you can claim Social Security benefits—is 67.

4. Fed Tax

The cut of your paycheck the federal government takes (other than for Medicare and Social Security). How much depends on your tax rate and the number of allowances you're eligible for. It is also affected by how much pre-tax money you spend on things like health insurance and other employee benefits, as well as by how much you put into retirement or 529 accounts, for example.

You can find this year's tax brackets here.

5. State Tax

The amount of your paycheck taken by the your state. Alaska, Florida, Nevada, South Dakota, Texas, Washington, and Wyoming do not have a state income tax, while New Hampshire and Tennessee only tax dividends and income from investments (not income from your day job).

6. City Tax

Many U.S. cities, including New York, Washington, D.C., and Detroit, charge an additional city tax.

7. SDI

SDI stands for State Disability Insurance and is a form of compensation for people who are injured off the job and are unable to work. It allows you to receive a percentage of your pay if you are on temporary disability leave or take time off under the Family and Medical Leave Act (for something like pregnancy or taking care of a sick relative).

8. Pre-Tax Deductions

Some pay stubs also break out how much pre-tax income you pay to things such as health insurance and 401(k) contributions. This is an easy way to check and see if you are putting enough into your 401(k) to receive your employer's full match.

9. Tax Filing Status

Your marital status will be listed, along with any allowances to which you are entitled. You stipulate these things on your W-4 when you start a job.

10. YTD Gross

Your gross pay multiplied by the number of pay periods thus far in the calendar year.

11. Current Deductions

The amount of money from your current pay period paid to the federal, state, and city government, as well as into your 401(k) and to insurance.

12. YTD Deductions

The total amount you've paid in taxes, to your insurer, and into your 401(k) thus far in the calendar year.

13. Net Pay

How much money actually got deposited into your bank account this pay period. Likely to be significantly less than your gross pay. Try not to worry too much if this is your first paycheck; as Ross told Rachel, "You can totally, totally live on this." It will (hopefully) only go up from here. (But if you're that unhappy about it, Money has written exhaustively on how to ask for more.)

14. YTD Net Pay

How much money has been deposited into your bank account thus far this year. Often a source of pain and consternation, sometimes a cause for joy. Can always be improved.

—Alicia Adamczyk

Have a question, comment, or suggestion? Email us at feedback@moneymail.com.