5 Essential Retirement Moves for Couples in Their 20s and 30s

You know your spouse's favorite food and go-to music, and maybe even the career he or she envisioned back in second grade. But do you know how much he or she has in a 401(k)? What about the mix of stocks and bonds across all your investment accounts? Looking far ahead, do you have an idea of when and where your spouse wants to retire, or how he or she dreams of spending time after leaving the workforce?

If you're like a lot of couples, the answer to most of these questions is probably "no." And some of what you think you know is likely wrong. That’s a problem.

Sure, retirement is decades away, and you and your spouse may feel you simply can't shoehorn much retirement saving into your budget. You may be grappling with modest incomes, steep rent, and student loans (the average college grad with debt carries a $28,950 balance)—and perhaps also making plans to buy a house and start a family.

But this is the critical time to lay the groundwork. What you do now has the biggest payoff because your dollars will have the longest time to grow. If together you can tuck an extra $100 a month into retirement accounts starting at age 27, you'll have an additional $240,000 at age 67, assuming your money grows at 7% a year. Start that at 37 and you'll add $115,000.

Here are five key moves:

Keep upping your game

Many employers automatically enroll new hires in a 401(k) plan, which sends a chunk of your pay into savings before you can get accustomed to having it in your wallet. But the most common auto contribution, 3% of pay, isn't enough to build a livable nest egg. Get in the habit of raising your contribution by at least 1% of pay a year. Your employer may make that easy: At 75% of plans administered by Fidelity, workers can sign up for such scheduled boosts.

Wherever you are is a good place to start, but aim high: "Your goal should be to save 15% of pay each year," says Tim McGrath, a Chicago financial planner. Socking away more dough may be less painful than you think because you contribute pretax dollars. So for someone in the 25% federal tax bracket, saving an extra dollar may reduce your take-home pay by just 75¢.

Read more: Money’s Ultimate Retirement Guide for Couples includes advice for duos in their 40s, their 50s, and nearing retirement. Plus, take our quiz to see if you and your spouse are on the same page.

When Tiffany and Michael Lucas, both 31, began dating six years ago, she was already a power saver, socking away 8% of her income. By contrast, Michael’s employer had automatically enrolled him in its 401(k) at 3% of pay, and he was happy to leave it at that. “I honestly didn’t care. I never really looked at it,” he says. As the relationship grew serious, Tiffany persuaded Michael to save more for their joint future. He boosted his 401(k) contribution to 9% of pay, and Tiffany is now at 14%.

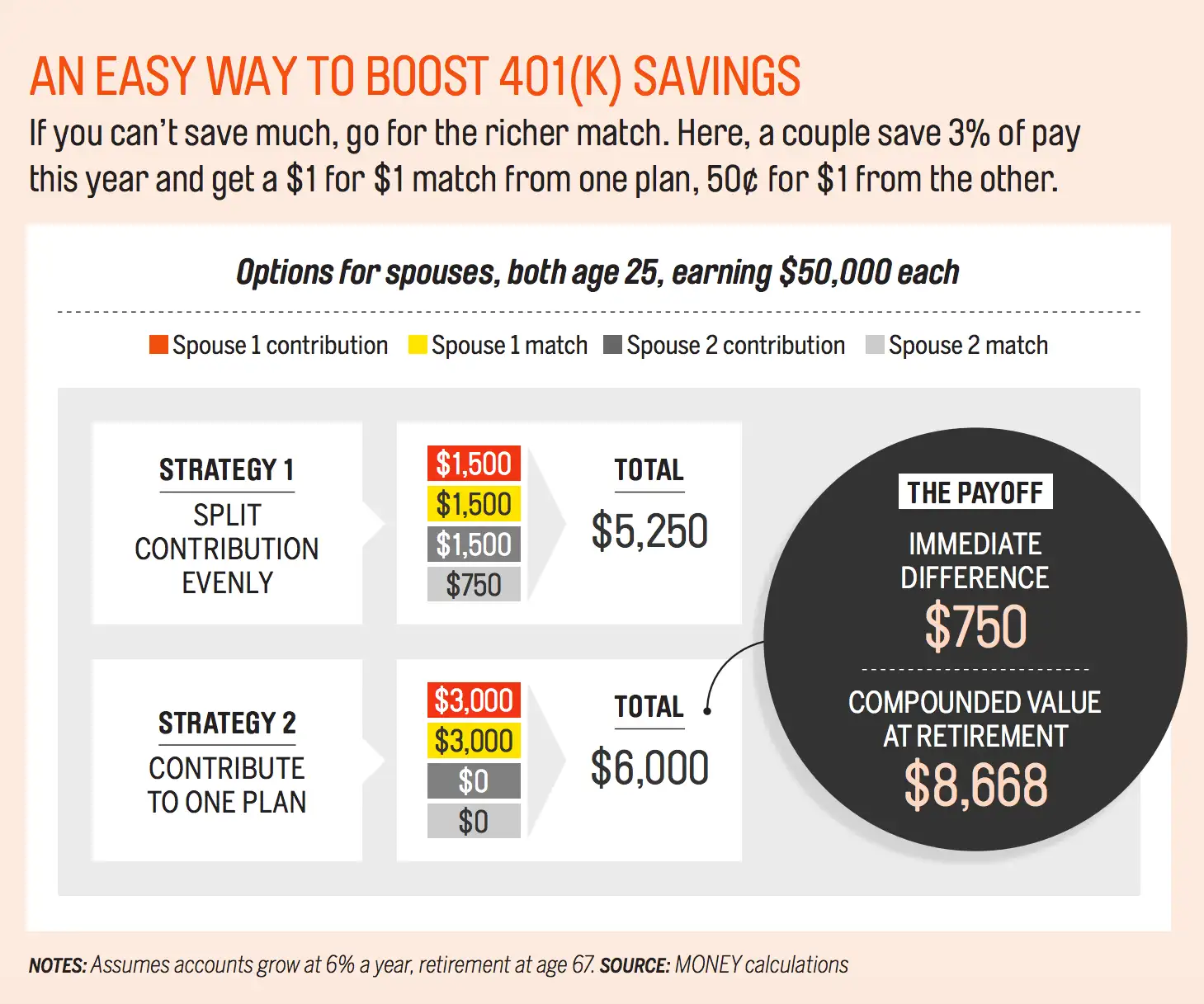

Don't be evenhanded

If at all possible, you want to get the full employer match. If cash is tight, direct more of your 401(k) dollars to the account with the bigger payoff. That could mean maxing out the $1 for $1 match in your spouse's plan before contributing to your 401(k), which offers 50¢ for each $1. For two 25-year-olds each earning $50,000 a year, being strategic with one year's 3%-of-pay contribution could add up to $8,700 at retirement, as shown in this graphic.

Add IRAs to your arsenal

What if one of you doesn't have a 401(k)? Opt for an IRA. Lean toward the Roth variety, even though you won't get a tax deduction now. (Income limits apply.) With a Roth IRA, you'll reap tax-free income later in life, when taxes are likely to be a bigger burden. You can also open a Roth to supplement your workplace retirement plan and have it do double duty: While you build a separate emergency fund, you have the ability to withdraw your Roth contributions at any time without penalty. You can also tap the Roth to help fund a first-time home purchase. For a nonworking spouse, you can contribute up to $5,500 to an IRA in 2016.

Weigh the big "R" in every big change

The richest pay boosts often come when changing companies. But if a job offer involves a lower retirement-plan matching formula, you'd want your new salary to more than compensate you for that change.

Meanwhile, more than three-quarters of mothers and half of fathers say they've passed up work opportunities, switched jobs, or quit to care for their children, according to a 2015 survey by the Washington Post. In deciding if one of you will scale back or stop working when you become parents, you'll no doubt check the impact on your budget. But also look for ways to minimize the hit to your future earnings and retirement preparations, such as by keeping a foot in the workplace as a part-timer or switching to a more family-friendly type of job.

If you decide to stay home, plan ahead for possible reentry. Keep your network current, even if that's just emailing work contacts to check in a few times a year, says Rosemary Haefner, chief human resources officer at CareerBuilder. And keep track of volunteer accomplishments that might look good on a future résumé, like overseeing a six-figure budget for your school's parent-teacher association or supervising a team of 20 on a major fundraising effort.

Read: The Single Most Important Money Talk for Couples

Run the race together

"Money is the No. 1 source of conflict in relationships," says Terri Orbuch, a therapist and researcher. Sometimes it seems as if couples are either arguing about money—like how much a spouse spent on [fill in the blank]—or not talking about it. Asked about their partners' pay, more than 40% of couples surveyed by Fidelity got it wrong.

The behaviors you adopt now will set the pattern for decades to come. If there's tension, address it head on. Talking about what money meant to each of you growing up may help you understand differences, Orbuch says.

Often one spouse naturally takes the lead in money matters. That's okay, says Brian Spinelli, a financial planner in Long Beach, as long as the other person is also involved and informed. It might help, for instance, if one of you pays the bills while the other handles investing. And just as you make a movie date with your spouse, make a regular monthly date to look over your numbers and talk about the inevitable issues that come up. (Bottle of wine optional.)

Read: Prenups Aren't Taboo For Millennial Couples

Kalynn Dresser, 27, says she controlled the finances initially because she knew more about saving and investing than did her husband, Nick, 29. "It was hard at times because I would say, "No, we can't afford that," and Nick would get upset," she recalls. The Asheville, N.C., couple worked over the next two years to boost his financial literacy and transfer some of the responsibilities to him. The change has made them both happier and put a lid on impulsive spending, she says.