Which Generation Has the Most Debt? It's Not Millennials

- How Much Is an Olympic Medal Worth? Record Gold and Silver Prices Are Driving Up Their Value

- Average Car Insurance Prices Expected to Hit $2,500 This Year

- Olympians Can't Pay Their Bills. Celebrities and Crowdfunding Are Coming to the Rescue

- Credit Scores Fall and Bankruptcies Climb in States With Legal Sports Gambling

- 8 Things People Have Stopped Buying (and Why)

Generation X, perhaps best known for being overlooked, stands out from the pack in one unfortunate way: debt.

By most measurements, Gen X is deeper in debt than other generations. Members of Gen X — born roughly from 1965 to 1980 — have the highest average debt stemming from student loans, credit cards and more.

Why does Gen X owe so much money? It’s mostly due to their current circumstances rather than particular personal finance decisions.

“To put it simply, many of these individuals are in an expensive phase of life,” Rod Griffin, senior director of consumer education and advocacy at credit reporting agency Experian, tells Money via email. “They may have mortgages and car payments on top of the ongoing costs of raising a family. They may be shouldering education expenses for themselves and/or their children.”

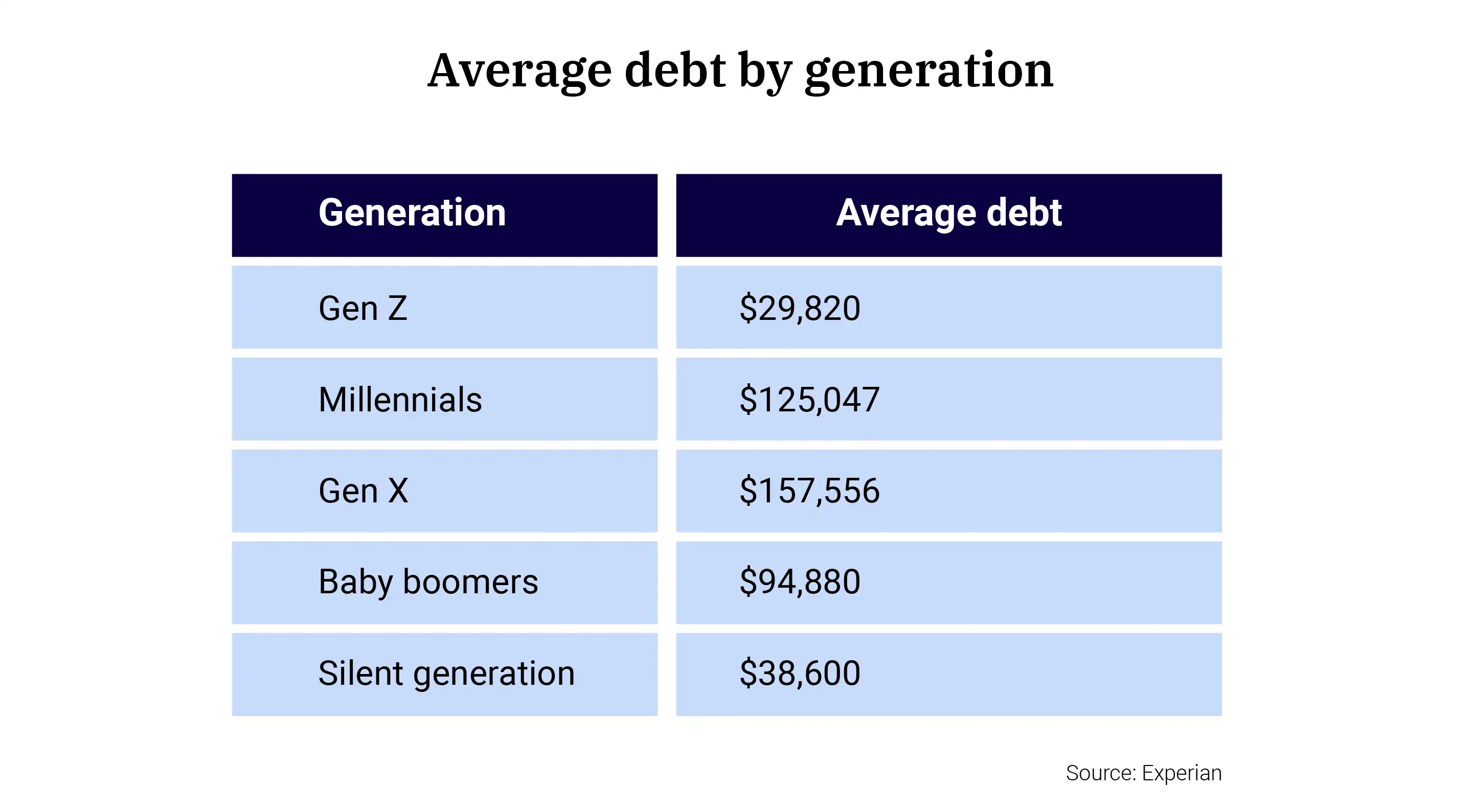

Here's how Gen X matches up in terms of debt levels with Gen Z (born 1997 and after) millennials (1981 to 1996), baby boomers (1946 to 1964) and the silent generation (1928 to 1945), based mostly on 2023 data from Experian.

Overall debt by generation

Though members of Gen X may be swimming in debt, they’re also in their highest-earning years right now — which certainly comes in handy if you have a ton of debt to pay off.

Another good thing: In all likelihood, Gen X’s debt will retreat as they get older and their kids (hopefully) move out and become financially independent.

“Generally, as consumers get into later stages of life, we see debt levels decrease and average credit scores increase. We expect to see a similar trend with Gen X as they age and begin paying off their mortgage, vehicles, etc.,” Griffin says.

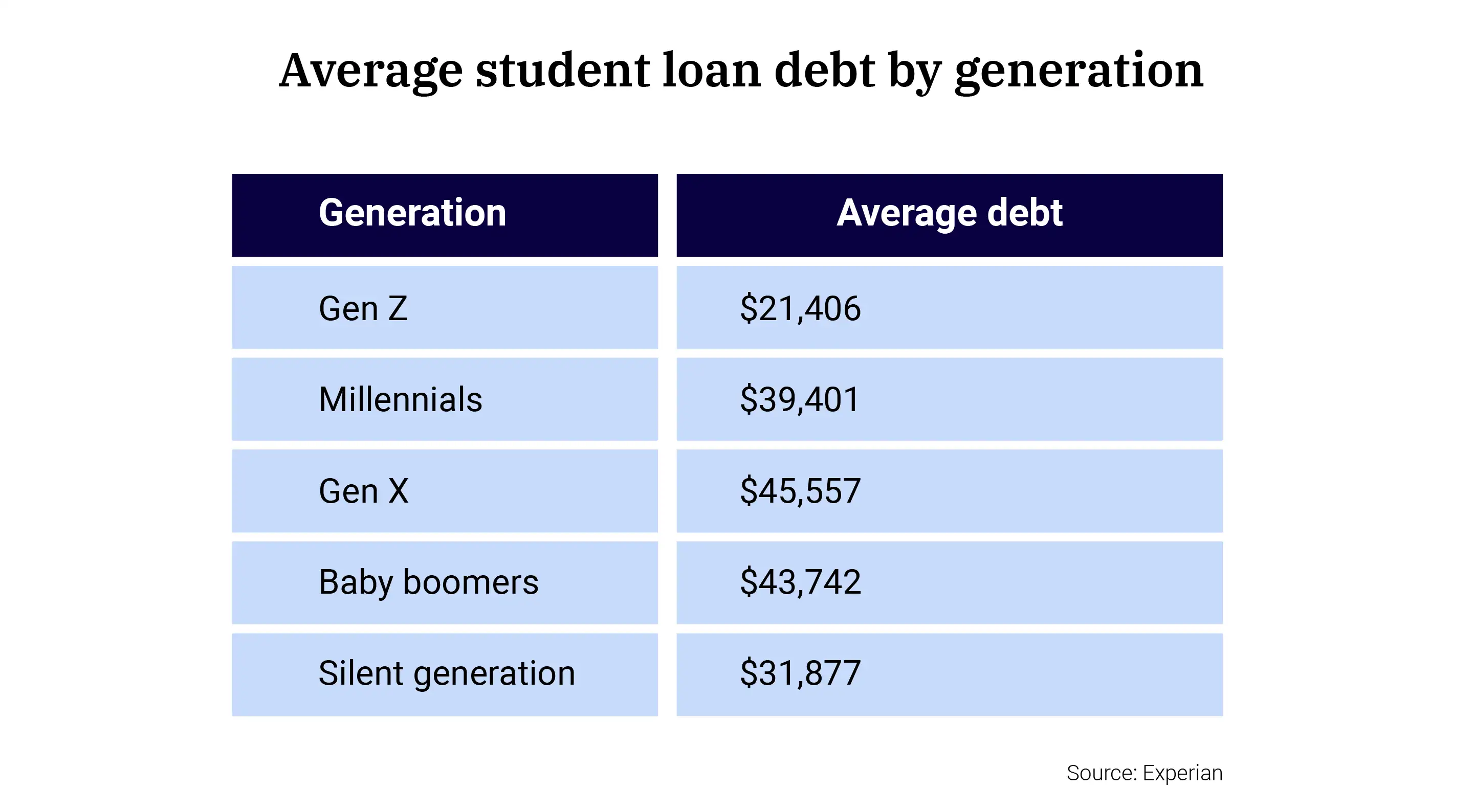

Student loan debt

Young people are more likely to have student loan balances: 24.3% of millennials and 20.2% of Gen Z are in student debt, compared to 14.9% of Gen X, 6.1% of boomers and only 1.4% of the silent generation.

But among those who have student loan debt, Gen X owes the most, on average.

(Note: The data below comes from Experian and is based on 2023 numbers. It’s unclear how debt levels may have been affected by the Biden administration’s many student loan forgiveness initiatives.)

At least Gen X overwhelmingly believes that going to college was worth the expense. According to a recent Debt.com survey, only 6% of Gen X says they regret taking on too much student loan debt, compared to 11% of millennials and 20% of Gen Z.

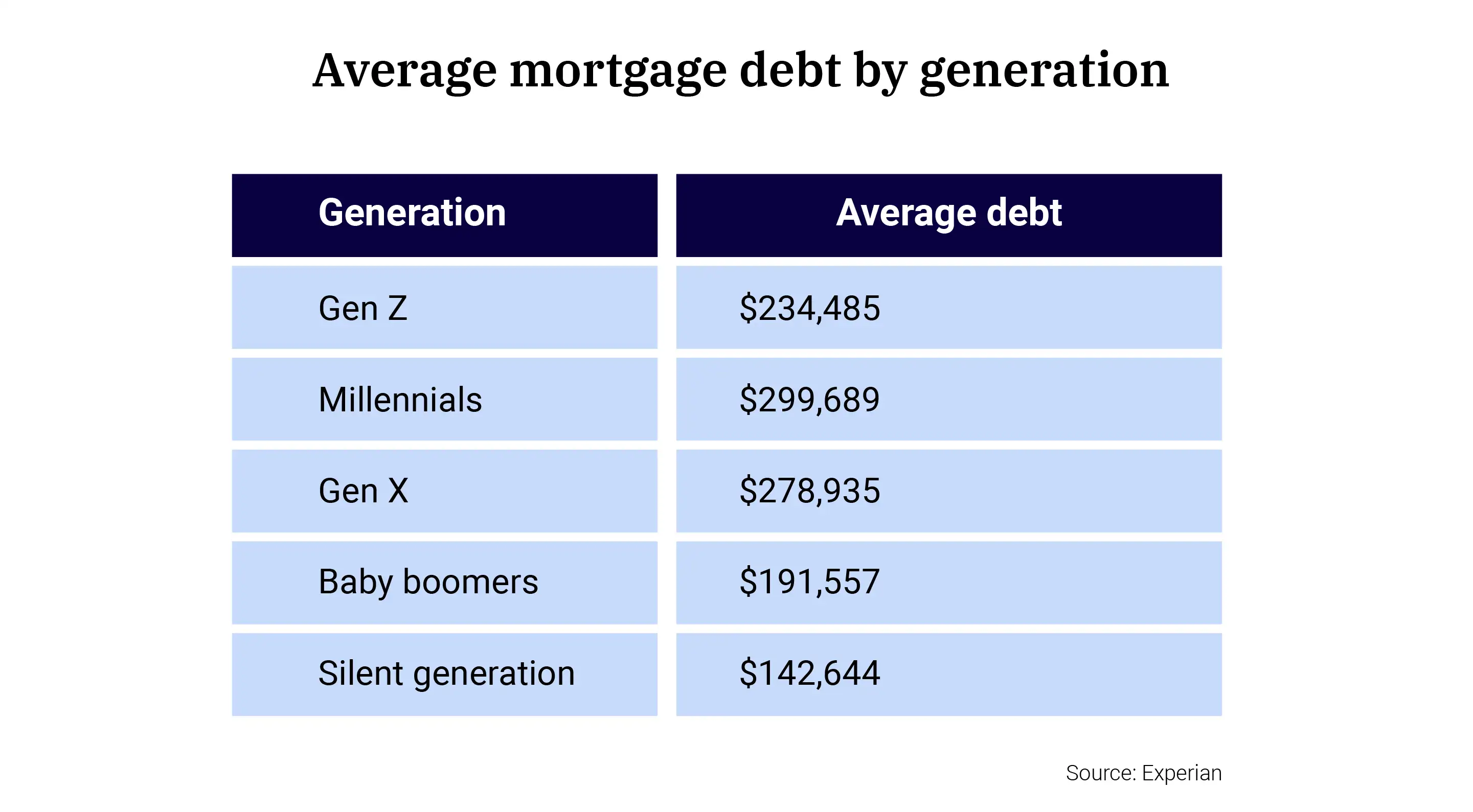

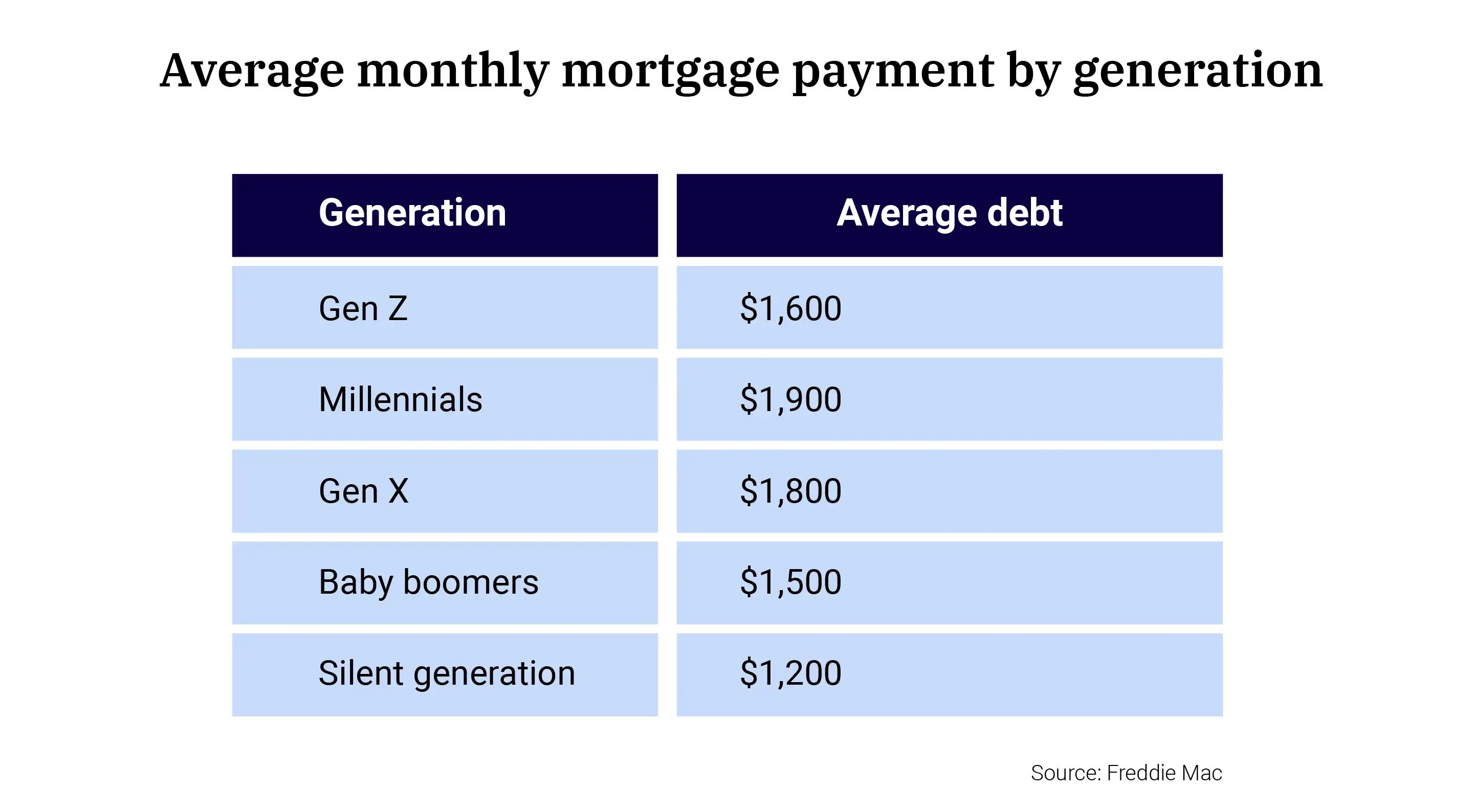

Mortgage loan debt

The average mortgage balance for each generation makes sense when you think about what’s likely to be happening in the lives of different groups right now.

Members of Gen Z are just entering the workforce and are facing a very expensive housing market. Basic starter homes may be all they can afford, so their mortgage payments are correspondingly small.

Meanwhile, millennials and Gen X homeowners could be on their second or third house at this point in their lives. Parents from these generations probably still have children living at home, so they need more space compared to young people who don’t have kids or older folks whose children are out on their own.

The older generations have had more time to pay off their mortgages or have even already downsized. In either circumstance, their mortgage balances would be smaller than the typical homeowner in their 30s or 40s.

While millennials and Gen X face the biggest mortgage bills, they’re also lucky enough to have the lowest mortgage rates.

According to a Freddie Mac report, the average mortgage interest rate at origination for millennial and Gen X homeowners is 4.0%, compared to 4.1% for boomers, 4.3% for the silent generation and 4.9% for Gen Z. The differences are largely a matter of timing: Members of Gen Z have been unfortunate to reach their prime homebuying ages over the past few years, when mortgage rates have spiked.

By contrast, “millennials entered the market when the rates were low, with 37% of all millennial borrowers’ purchases occurring in 2020 and 2021," the Freddie Mac report explains. “While 25% of all Gen Xers’ purchases were in 2020 and 2021, Gen Xers who already were homeowners took advantage of low rates and refinanced during the low-rate period.”

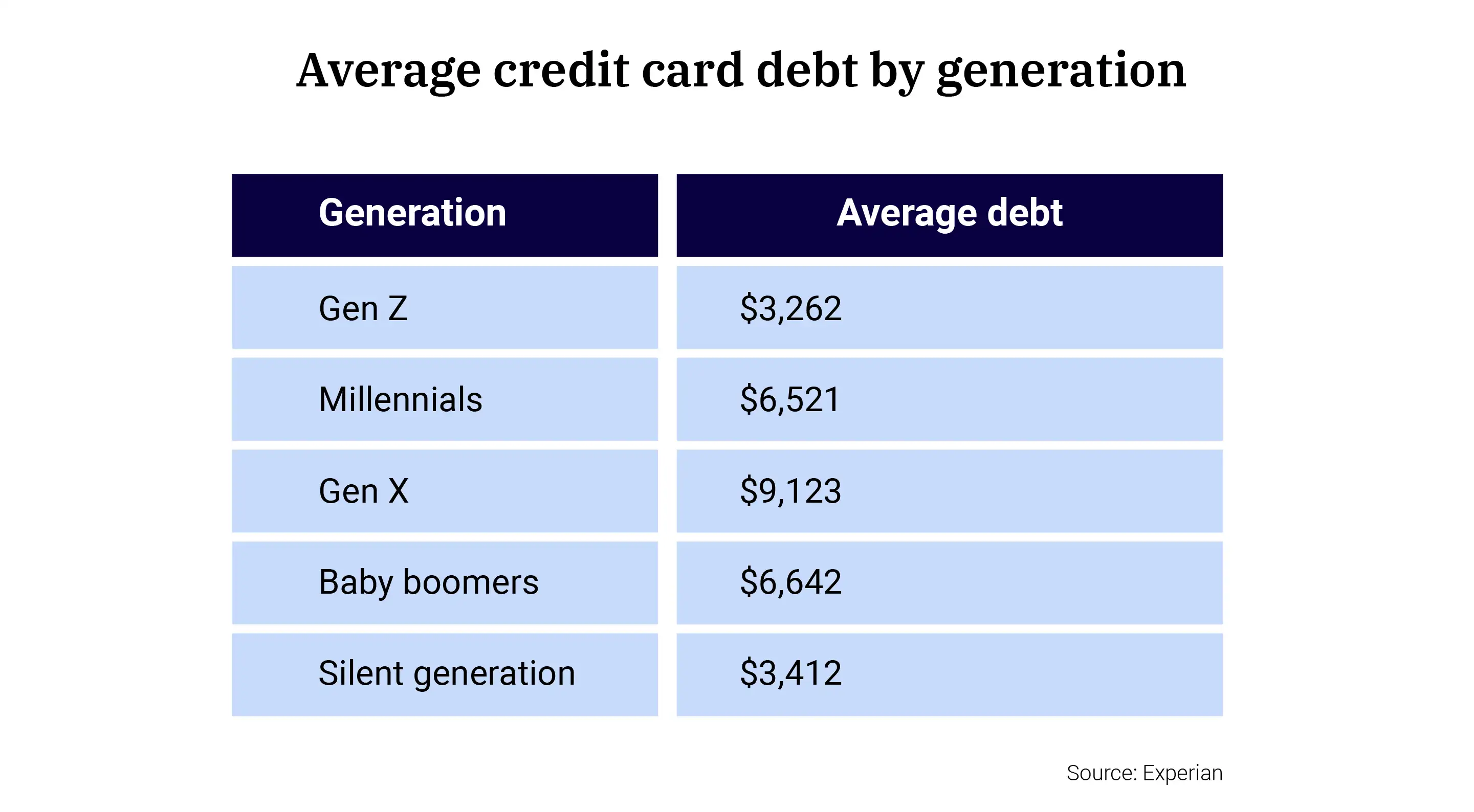

Credit card debt

Credit card debt levels follow a similar pattern to other debt categories, with Gen X leading the pack.

While Gen X has the highest average debt, millennials are most likely to wish they didn’t spend so much on their cards. Just over one-quarter of millennials say they regret piling up their credit card debt, versus 19% of Gen X and Gen Z, per Debt.com.

Find a Credit Repair company that works for you

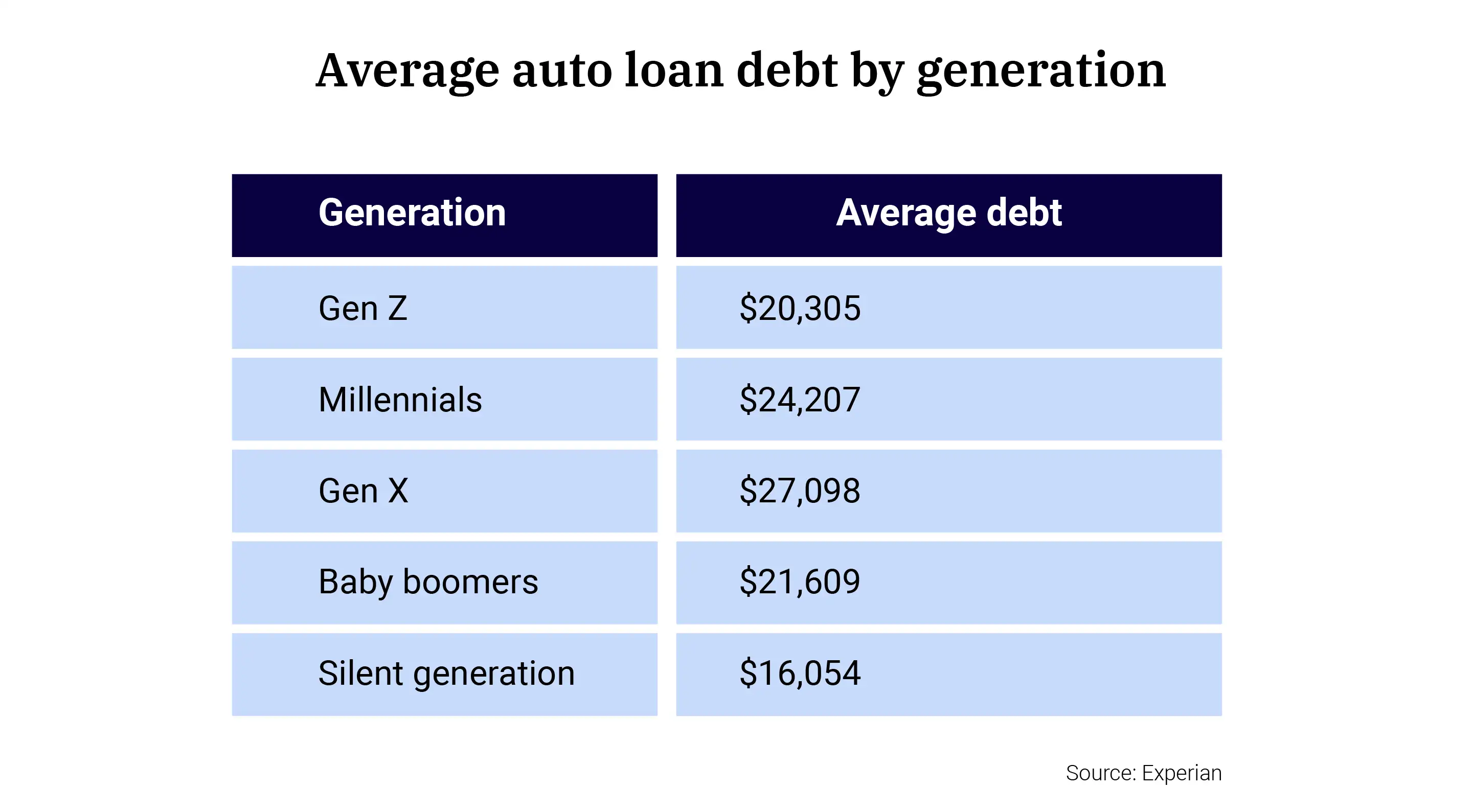

Auto loan debt

It’s largely the same story for auto loan debt. Once again, those Gen Xers have the highest debt levels, likely because they need bigger vehicles (think: SUVs) and more of them (for teenage drivers).

More from Money:

Here’s How Much Debt the Average American Has