There's an Investing Gap That Costs Women Up to $1 Million. Here's How to Fix It

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Today, gender equality is in the spotlight like never before. The #MeToo movement has encouraged countless women to share their stories about being harassed at work—myself included. Powerful men have lost their power, while powerful women (hi, Oprah) are putting their platforms and their money into stopping workplace harassment and abuse. It's been incredible. And it's just the beginning.

This movement has also highlighted the importance and power of being financially stable. Get-your-hand-off-my-leg stable. Take-this-job-and-shove-it stable. Live-my-best-life stable. Have-as-much-money-as-the-guys-do stable.

Here, we have a ways to go. Maybe you've heard of the gender pay gap. Frustrating, right? And costly. But there are more gaps at play: Women pay more for the debt they carry than men, and they don't invest as much as men do. As a result, women retire with two-thirds the money of men…even though we tend to live years longer. Don't believe me? Check the gender mix at your local nursing home: 80% of women die single, and they're also 80% more likely to be impoverished in retirement than men. Yuck.

So there's work to do. You may not be able to close all the gender money gaps immediately, but you can take action right now, and you should. It can change your life.

What is the gender investing gap?

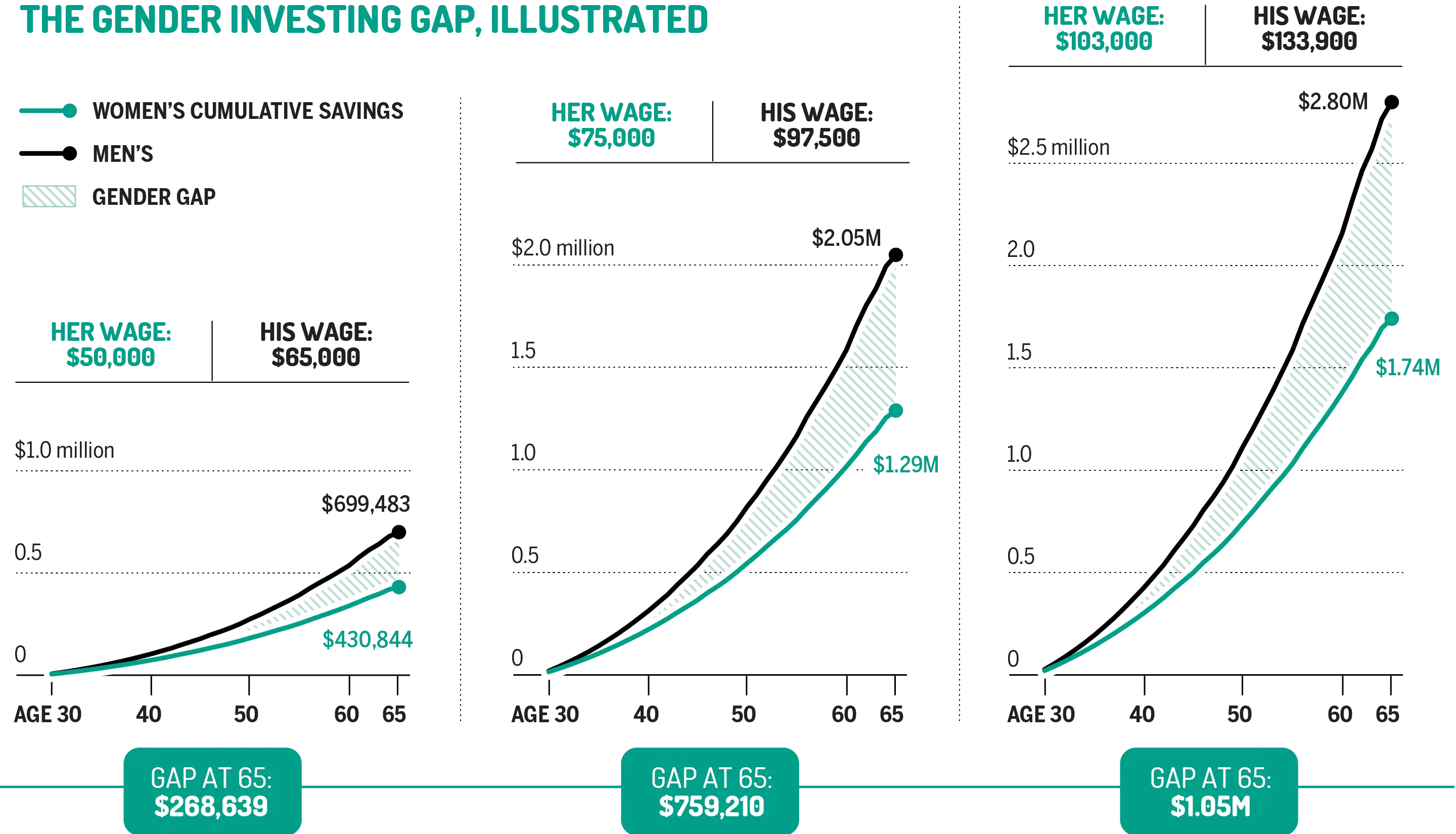

Simply put, women don't invest as much as men do. And they don't invest as early as men do, either. Of all the assets women control—both inside and outside their portfolios—they keep a full 71% in cash, according to a survey by BlackRock, whereas men hold 60%. Cash may feel like zero risk, but it also has zero potential to grow as stocks do over time. And even with low inflation, the purchasing power of that cash will decline over time. So the price of certainty you get with cash is high.

How high? We recently published the Ellevest 2018 Money Census, in which we asked 1,000 women about all things money. Nearly half of women weren't even aware there was an investing gap. And when asked to estimate how costly it was to them, their average guess was $113,000.

Not even close. We ran some projections based on the wage gap, typical asset allocation strategies, and a gender-specific salary curve. The true cost for the average woman at the time she retires may run two to seven times that amount. Depending on your salary and the market's performance, the real cost of the investing gap over a 35-year career span could be more than $1 million. Yes, I said a million.

Conventional wisdom "blames" women for this gap. We receive messages that we're not as good at math as men; we're not as good at investing. Um, no. Studies have found that once women do invest, they outperform men by nearly one percentage point a year. This was confirmed recently by Fidelity, which analyzed the performance of 8 million retail clients in 2016. Typically women outperform because they don't overtrade, panic in down markets, or pay too much in fees.

How to close the investing gap

This is going to sound a bit like a Nike commercial: Just do it. Find an advisor who feels right for you—and don't settle. Ask friends, ask work colleagues, search the Internet, do some digging online.

First make sure you ask any potential advisor five crucial questions. These include making sure an advisor puts your interests before his or her own, keeps costs low (below 1% for human service and 0.5% or less for digital), doesn't hide fees, doesn't chase the latest hot trends, and diversifies and personalizes your portfolio to meet your goals.

The best place to start investing is in a 401(k) retirement account, if your employer offers one. The tax advantage will help your money grow faster, and if your employer provides a match, all the better! (That's free money.) If you have the ability to contribute up to the match, do that first—since your contributions are pretax, they can help lower your tax bill. Next, look to an individual retirement account outside work. IRAs have a further tax benefit, but not all of them have the same effect on your tax bill. IRAs are great if you want to put more toward your retirement. If you don't, then invest in outside brokerage accounts.

A key point: I hear from a number of women that they don't invest because they are nervous about the stock market and potentially "losing everything."

At Ellevest, we've found (and research confirms) that women are not so much risk-averse but risk-aware—meaning that they want to thoroughly understand a risk before they take it on. And once they do? A study from the University of California at Berkeley describes women as "rational" investors, meaning that they take on smart risks, and the women in the study outperformed the men, whose overtrading due to overconfidence was a less successful move in the long run.

That's why a diversified, low-cost investment portfolio is important, so you're not investing in just the stock market.

Making investing a habit—a bit out of every paycheck—is also smart and may be a means of further reducing risk. That's because sometimes you may be "buying high," and sometimes you may be "buying low." But over time, these may even out…and reduce the time it can take for your portfolio to recover from any market downturn (since during the stock plunge, you'll be "buying low").

What is the gender debt gap?

Okay, brace yourself for this one: In some cases, women are carrying more debt for the exact same things that men do…even though study after study shows that women are less likely to default.

A couple of examples: Women tend to have higher average loan-to-value ratios on their mortgages, which means they take on more debt than guys for the same house. As for student loans: Women make up 56% of higher-education students, but hold 65% of all student debt.

Women also pay more for credit card debt. One study by the FINRA Investor Education Foundation found they pay half a point higher annually on their cards. Another study from the Urban Institute found that single women pay higher rates on their mortgages than single men do.

Why the heck would that be? For student-loan debt, 26% of college students are parents, and 71% of those parents are women. So additional childcare costs are probably part of it. But the reasons are difficult to pin down, especially given that, by many reports, women have higher credit scores than men do overall.

Regardless, the reality is more debt and higher costs. And because of the gender wage gap, less earnings to pay it off. (That sound you may hear is my head banging against a wall.)

If you're a woman struggling with debt, you're not alone: In the U.S., credit card debt just rose to a record $1.023 trillion. Paying off debt was a top-three goal of women in the Ellevest 2018 Money Census, across all ages and regions. The women in our census were far more likely to be dissatisfied with their current level of debt than men.

Being frustrated is one thing; knowing when to be truly concerned is another. If you have a debt-to-income ratio of more than 36% of your gross income, you're going to be stuck "treading water"—unable to invest and pursue your other financial goals until you pay it down.

How to close the debt gap

Let's face it: Paying down your debt will take some sacrifice and focus. But it's worth it, since it can drag you down from achieving your goals.

First on the chopping block: credit cards. If you've heard of "bad debt" vs. "good debt," credit card balances are the bad debt. You should pay this debt off first—in fact, ASAP—because credit card interest rates run high. The current average annual interest rate is above 16% (some are lower, some way higher).

How much does credit card debt cost you? Find out by multiplying your interest rate by your outstanding balance to get the total you owe the company, simply as a thank-you for lending you the money. (You may need a glass of wine for this part.)

Then pay that down as quickly as you can each month, shooting for more than the minimum. That may mean fewer dinners out, cutting back on a vacation, wearing that coat one more season. But getting that monkey off your back can be worth it.

Don't close out a card account with an open balance, because that can hurt your credit. But do consider transferring your balance to a card that charges 0%. Then use your newfound "savings" (of not having interest payments to make on that 0% card) each month to pay that balance down. Most cards charge 0% only for a short time (usually up to 15 months), so do the math to be sure you can actually pay down your debt substantially at 0% before you're saddled with a giant rate hike.

Then there's "good debt"—or obligations that you don't need to pay down right away. At Ellevest, we define "good debt" as a loan that represents an investment in your future (a student loan, a home mortgage) and that charges an annual percentage rate, or APR, of no more than 4% to 5%.

"Good debt" does not necessarily need to be paid back before it's due, in part because investing money in a diversified, low-cost investment portfolio is likely to earn you a greater return than this debt will cost you over time.

But do be sure to make payments on your good debt on time and check periodically for opportunities to lower your payments. For example, if you have student loans, put them on autopay, which can help you save 0.25% from most lenders. And look at sites like Earnest.com and CommonBond to refinance.

It also may make sense to refinance your mortgage, if you can lower the interest rate on your home loan enough for it to be worth the upfront cost and the time suck it can take. Usually it's only worth exploring if you plan to stay in your house long enough to pay off the fees from the new loan and you can get a rate at least 1% to 2% lower. (Refinancing is something to look into right now, by the way, before interest rates go up again.)

Of course, the thing that would really help women pay off their debt is having a 25% bigger paycheck…by closing the gender pay gap.

What is the gender pay gap?

It's real, and at the very least people are beginning to understand that the average woman makes between 78¢ and 80¢ for every $1 a man makes in the same job. To a woman earning $85,000 a year, that translates into lifetime costs of hundreds of thousands of dollars. The gap is not as bad for millennial women (at closer to 90¢), but it's worse for women with disabilities (72¢), black women (63¢), and Latinas (54¢).

The good news? Our Ellevest 2018 Money Census indicated that 61% of men now recognize the pay gap. The bad news? At this rate, it won't close until 2119.

How to close the pay gap

This is one of the toughest gaps to close, because it's not fully under your control. But the best way to raise your pay is to make the best possible ask.

Start by researching how much your job is worth using the numerous websites that are popping up, such as Comparably, Glassdoor's Know Your Worth, Hired.com, and GetRaised. Then schedule a talk with your bosses ASAP to define what success looks like for you and your division.

Find common ground on the metrics you and your bosses will track. Ask how they want to see you grow professionally, and what success looks like for the company as well. (If you just did year-end reviews and don't have the answers for all three, ask for a follow-up conversation.)

Right before review time, update the goals you've met and how you've grown. Practice talking about them at home, if you might get flustered. (I've been doing this for a lot of years, and I still get flustered.) Then go ask for that raise or promotion, even if you don't think you're 100% ready. According to one study, women ask for a promotion when they're 100% ready, and men when they are just 60% ready. Hmm.

Don't give up if you get a no. Ask for non-money perks: flextime, a new title, pay reevaluation next quarter, or mentorship by or a project with a senior exec. They're valuable in themselves, but they also get your boss in the habit of saying yes to you, and that will help you get that raise next time. Remember, this is a lifetime gap you're working to close!

Now: If you tick all the ask boxes and still come up with bubkes, that's a huge sign that this company is just not that into you. If so, you're at risk for yet another gap (yep, there are more): the gender work achievement gap.

You've heard the stats that there are more CEOs named John in the U.S. than there are women CEOs? You don't want to fall behind the Johns where you work, and that's what will happen if your company isn't willing to invest in you. Fortunately, you're now armed with lots of bragging points and a great sense of the market value of what you do, which will help you seek out the next great opportunity and negotiate your new offers like a pro.

Women won't be truly equal to men until we're financially on par—so go start closing those gaps! As Ellevest investor and tennis champ Venus Williams once said: "There's nothing more impressive than a woman who knows her power."