These Are the Low-Risk Stocks With the Best Prospects Now

- It's a Huge Day for the Stock Market. What You Need to Know About History's Longest Bull Market

- The Best Performing Stock of This Bull Market Is Up Almost 39,000% — and You've Probably Never Heard of It

- Worried About a Stock Market Crash? 5 Ways to Keep Your Money Safe

- The Stock Market Is Plunging Again. This Time, It's About Trump

- A 100-Year Curse on GOP Presidents Might Explain Why Stocks Are Tumbling

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

After plunging 13% in the summer and rising 14% in the fall, stocks sank 13% in early winter only to surge 12% since mid-February. Pass the dramamine. To calm their nerves, investors have traditionally turned to "widows and orphans stocks," rock-solid shares of the biggest dividend-paying companies—firms destined to dominate their industries for years. That sounds like a smart way to ride out today's choppy markets. Yet in the global financial panic less than a decade ago, the strategy didn't always work out. Even stodgy giants like General Motors, Merrill Lynch, and Lehman Brothers were forced into bankruptcy, to a sale, or out of business.

That experience shouldn't dissuade you from searching for Steady Eddies this year. Stocks that offer you a smoother ride generally end up outperforming in the long run. But you'll want to broaden your definition of what widows-and-orphans stocks are—and what role they can play in your portfolio. To figure out how, Money gathered industry experts at the World MoneyShow conference in Orlando in March. During that discussion the panelists identified the following five guidelines for finding modern-day widows-and-orphans stocks.

Rule No. 1

Focus on quality first—stability will follow

Widows-and-orphans stocks are supposed to be safe enough even for a widow or an orphan to own—in any type of market. "The traditional definition pointed you to names like General Electric , Procter & Gamble , or one of the big drug stocks," says John Fox, chief investment officer at Fenimore Asset Management. And those are precisely the type of blue chips being talked up in this aging bull market.

Trouble is, when the S&P 500 index sank 37% in 2008 in the global financial panic, shares of GE and Merck plunged more. Those two supposedly safe bets each lost about half of their value in a year, hardly something you would wish upon a widow or an orphan with little appetite for risk. It goes to show that the only investments that come with absolute assurances are U.S. Treasury bonds.

Your best moves:

Look for stocks that are stable enough. "Nothing's immune all the time," says Jack Ablin, chief investment officer for BMO Private Bank. After the Clinton administration proposed health care reform in 1993, even the biggest health care shares were hit, Ablin notes. In 2000 it was the tech giants' turn, followed by big banks in 2008 and Big Oil last year. The trick is to find shares stable enough so in the event of a downdraft, you're less likely to panic and sell, making a bad situation worse.

Go with stocks that lose less. A smart way to identify stability is to focus on high-quality businesses. "There's an old saying," says Sam Stovall, U.S. equity strategist for S&P Capital IQ. "When the seas get rough, sailors prefer better-made boats." For good reason. When the broad market sank 5.5% in the first two months of this year, the S&P 500 High Quality Rankings index held its ground. And in months when stocks fell over the past five years, high-quality shares lost about 30% less, according to Morningstar.

Follow Buffett's lead. Look for companies with competitive advantages in their industries—what Warren Buffett calls "wide moats"—that keep rivals at bay, Fox says. Then look for businesses with strong balance sheets marked by little or no debt and solid cash flow and earnings. One profit measure Fox relies on is return on equity, which gauges how efficient companies are at generating net income. The historical average ROE for U.S. stocks is roughly 10%, so you want to look for stocks above that.

You can find such companies in PowerShares S&P 500 Quality Portfolio , which is on our Money 50 recommended list. Top holdings include Gilead Sciences, the drugmaker with patent protection for its leading hepatitis and HIV treatments; Visa, with no long-term debt; and Johnson & Johnson, which sports an ROE of around 22%.

Rule No. 2

Size doesn't matter as much as you think

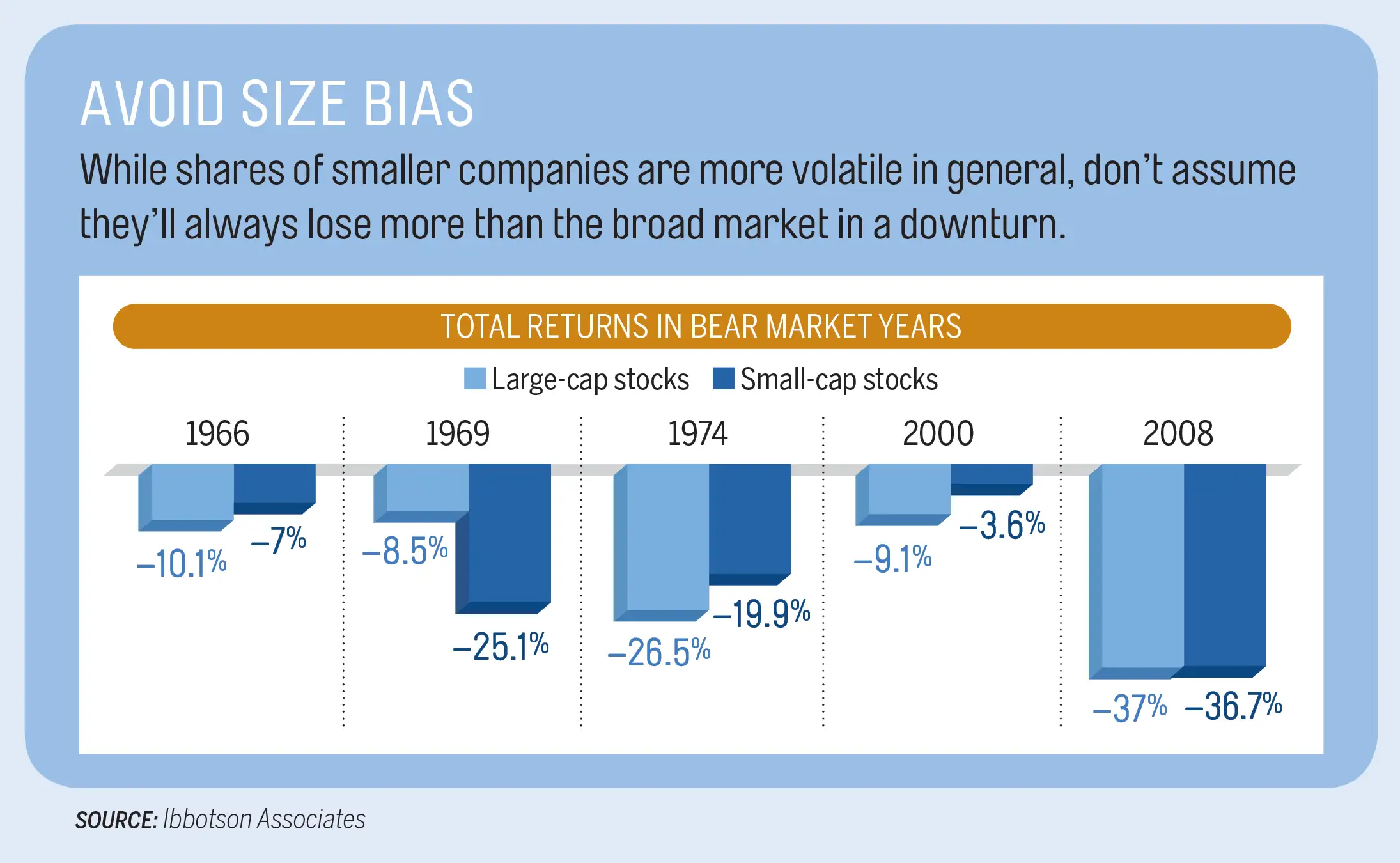

Call it the Titanic theory of investing: You've probably been told that owning the absolute biggest and most dominant companies is the best way to find safe and stable stocks. Alas, that's not necessarily been true in recent bears. In the 2000–02 tech wreck, for instance, the S&P 600 small-stock index fell only 22%, less than half what the broad market lost.

Your best moves:

Diversify by size. No one is saying go small with your entire portfolio. But a simple way to hedge your bets on big Steady Eddies is to add smaller high-quality stocks to your mix. "A lot of small and midsize companies are well-established businesses run by managements with a long track record," says Fox.

Be boring. While small-stock investors usually gravitate to highfliers or startups, avoid sexy, says Fox. Take Brown & Brown , a Florida-based property and casualty insurance brokerage that lost only a third of what the market did when stocks slumped from November to February. "For every dollar of sales they generate, they bring in 30¢ profit, which is phenomenal," says Fox. "They generate $400 million a year in cash, and they need to invest about $20 million back in the business, so the rest is for dividends and shareholders."

Another example is Donaldson , a Minneapolis manufacturer of filters and parts for trucks, bulldozers, and turbines. The stock fell about a third less than the S&P 500 last summer and this winter, as well as in the 2008 crash. Donaldson has an above-average return on equity of 24%, nearly double that of industrial equipment giant Caterpillar.

You can own smaller high-quality stocks through Fox's FAM Value Fund , which lost eight points less than the S&P 500 in 2008 and made money in the 2000–02 bear. During Fox's tenure with the fund over the past 15 years, FAM Value has returned 8% annually, which is more than two percentage points better a year than the S&P 500.

Rule No. 3

Valuations trump stability

There's no question investors covet Steady Eddies in volatile times. That's the problem right now. So-called low--volatility stocks—defensive shares that literally bounce up and down less than the broad market—"were trading at around a 50% discount to the broad market 15 years ago," Ablin says. But they've become so popular in recent years "they're trading at a 20% premium." And history shows lofty prices will weigh on even the highest-quality stocks.

Your best moves:

Bypass the bandwagon. "Beware of low-volatility ETFs because they're going to show you a fantastic track record" to attract new business, Ablin says. It's working. So-called low-vol funds and ETFs have pulled in more than $21 billion since the start of 2014, at a time when equity funds in general have seen net redemptions of nearly $50 billion. "They'll argue this performance is going to continue," Ablin adds. "But investors jumping in at this time will likely be disappointed" because of those high prices.

The average stock in the iShares MSCI USA Minimum Volatility ETF trades at a price/earnings ratio of more than 20, vs. less than 17 for the broad market and the S&P 500 High-Quality Rankings index.

Search for neglected widows and orphans. High-quality stocks that are steady by virtue of their financial and competitive strength are less expensive than low-volatility shares. Cheaper still are quality stocks in sectors of the market that have been beaten up lately, such as industrials and energy.

Ablin says a prime example is Whirlpool , which manufactures Whirlpool and Maytag appliances and KitchenAid products. The shares trade at a cheap 11 P/E, in part due to a pullback last year on fears the strong U.S. dollar would hurt Whirlpool's sales abroad.

Yet the stock has outperformed the broad market by four percentage points annually over the past 15 years and seven points a year over the past five. And annual earnings growth is expected to accelerate from 10% to nearly 17% over the next five years.

Another stock popular with quality-minded investors is Emerson Electric , a leading manufacturer of electrical products and industrial automation services. Because it has some exposure to energy companies, Emerson shares took a hit in 2015 as oil prices slid. But this company has boosted dividends for 59 straight years. And its return on equity is still 30%. So even in tough times, the company is more efficient at making profits than 80% of the S&P.

Rule No. 4

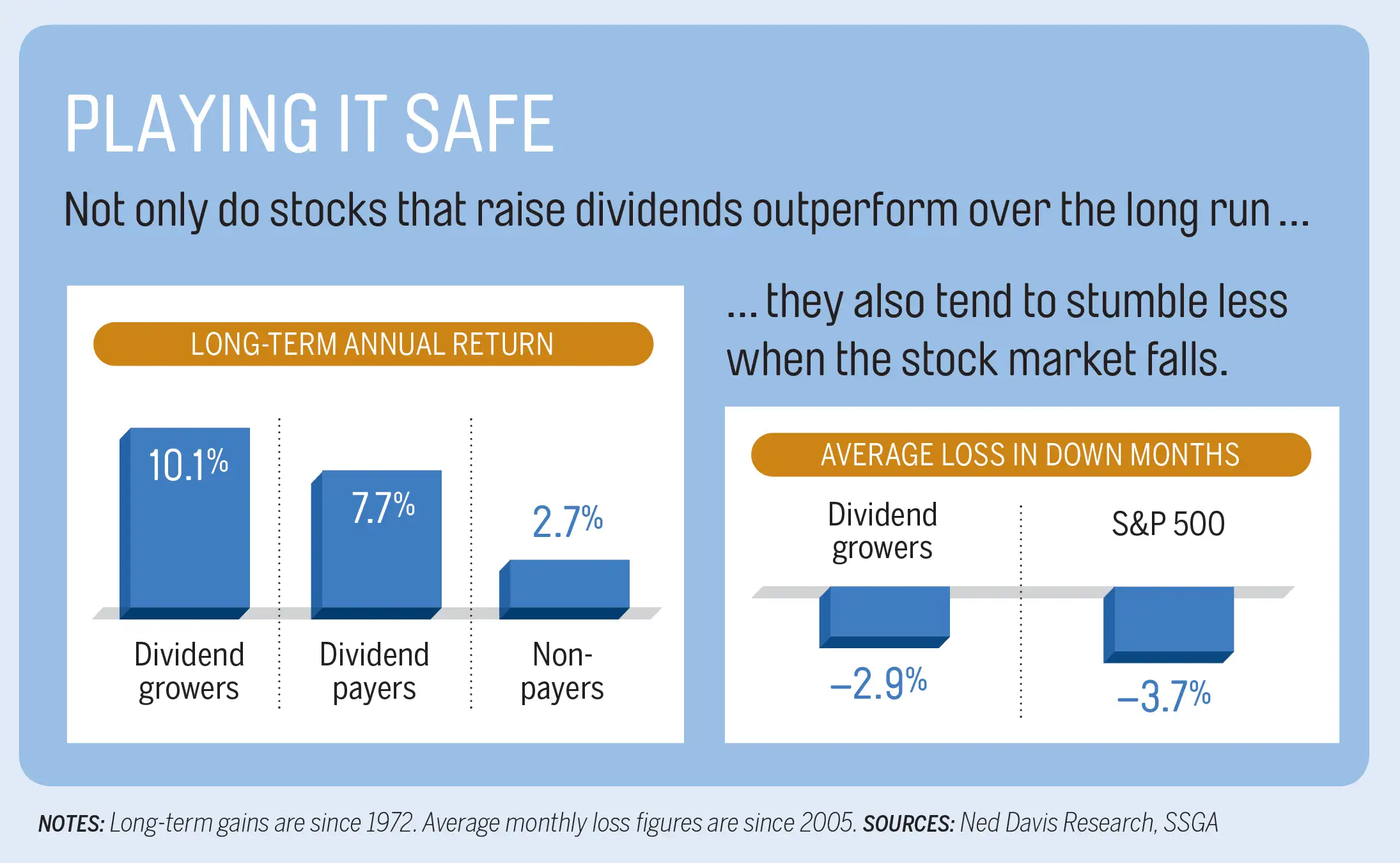

Favor dividend growth over high yields

Generous dividends have long been associated with widows-and-orphans stocks on the theory that "if you're a widow or orphan, you're probably not working and you've got to eat, so you'd want a good dividend payout," says Stovall. However, an extremely lofty yield can be just as much a sign of financial danger as safety. That's because a stock's yield may be high not because its payouts have grown recently, but because the stock price got crushed.

Your best moves:

Use payouts as a tool. Rather than thinking of dividends as just a form of current income, use them to judge the financial strength of a business—and therefore a stock's safety. "Dividends themselves are not a source of value," says Fox. "Cash flow is a source of value. Dividends are a choice of what management does with its cash."

Demand a raise every year. "You want dividends that are almost bond-like," says Ablin. But more than that, you want to invest in firms that consistently boost payments to shareholders even in tough times. If you can find that trait among stocks with a decent current yield, all the better. "Look at Exxon Mobil," says Stovall. "I don't see the company cutting their dividend. If you have a track record of raising dividends in each of the last 35 or so years, that's going to be the last thing you do."

If you invest strictly through funds, go with ProShares S&P 500 Dividend Aristocrats . The ETF tracks the S&P 500 Dividend Aristocrats index. That's a group of blue-chip companies that have increased their shareholder payments for at least 25 consecutive years, including Emerson Electric, Exxon Mobil, and Johnson & Johnson. When the Dow Jones industrial average sank 13% from November through mid-February, this ETF fell only 7%.

- Read next: Why You Should Invest Like Your Grandparents

For a fund that offers you exposure to the broader U.S. market—including some small- and medium-size stocks—check out SPDR S&P Dividend ETF , which is on our Money 50 list. In 2008, when the S&P 500 fell 37%, this high-quality stock fund lost 14 percentage points less than the market.

Rule No. 5

Use mental tricks to help stay the course

The fact that even the Steadiest Eddie stock can lose money is bad enough. But investors often make matters worse by bailing out of supposedly safe stocks and funds at the worst time. "The key to making money in the stock market is staying in the game," says Fox.

That's a lesson lost on many investors. Consider this: Over the past 15 years the Fidelity Dividend Growth Fund, which invests in high-quality companies with the financial strength to consistently raise their payouts over time, has generated total returns of about 5% annually. But by jumping in and out of the portfolio, the fund's investors have earned about two percentage points less a year, according to Morningstar. In effect, their impatience turned a widows-and--orphans-type stock fund into a slow-growing bond.

Your best moves:

Look at the dividend, not the stock price. If you need help staying the course, try this mental trick: "Separate the dividend from the principal," says Ablin.

How? Mentally organize your sources of gains into buckets. The first bucket is for price appreciation. The other is for your stock dividends. In the event of a market downturn in which your high-quality shares lose value, don't even look at the price bucket, says Ablin. "Just forget about it as long as you're comfortable that the company has the wherewithal to continue to pay the dividend and potentially raise it." While providing you income, rising dividends should give you confidence in the company's ability to eventually recover.

Remember that time is on your side. While downturns can feel excruciating, it has typically taken less than two years for equities to recover from the effects of a bear market (and just 11 months following mild bears). As long as your stocks keep paying you during this stretch, you'll know your shares will eventually get you where you need to go. At the end of the day, isn't that what widows-and-orphans stocks are supposed to do?