Dow Races Past 18,000

- This One Indicator Has Predicted Every Recession Since 1960—and It's Flashing a Warning

- The Stock Market Is Plunging Again. This Time, It's About Trump

- A 100-Year Curse on GOP Presidents Might Explain Why Stocks Are Tumbling

- The One Business Advisor President Trump Can't Afford to Lose Is Reportedly 'Disgusted' by Charlottesville Response

- This Chart Shows How Trump's Stock Market Gains Compare to the Last 13 Presidents

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

The Dow Jones industrial average climbed above the 18,000 level for the first time ever, shortly after the government released a report showing the U.S. economy grew at an annual rate of 5% in the third quarter—much faster than was initially thought.

The report also pointed out that consumer spending increased faster than expected, a sign that the improving labor, stock, and housing markets are finally being felt by American households.

Given this fact, conventional wisdom says the market is enjoying a normal Santa Claus rally. But conventional wisdom is wrong. Here's why:

At the end of most years, stocks tend to surge for reasons of good tidings and good cheer. This year, however, the bulk of the near 1,000-point rise in the Dow that began a week ago has really been driven by bad news around the world.

As economies in Europe, Asia, and Latin America have all slowed more than expected, expectations for global growth have sunk, driving down oil and commodity prices. In fact, crude oil prices have tumbled by nearly half, to around $61 a barrel since the summer.

Brent Crude Oil Spot Price data by YCharts

For American consumers, this is an early present from the North Pole. The average price of regular-grade gas in the U.S. has fallen to $2.47 a gallon, the lowest point since 2009, which leaves more money to stuff into Christmas stockings at this time of the year.

Yet for large parts of the rest of the world, falling oil prices and the slowing economy spell trouble.

Falling energy prices, for instance, are wreaking havoc on the budgets of emerging economies that are dependent on oil revenues to maintain their finances. Russia, Algeria, Iraq, Iran, Nigeria, and Libya all require oil prices above $100 a barrel to keep their debt/gross domestic product ratio from rising, according to a recent report from Goldman Sachs.

Even Middle Eastern oil producers such as Kuwait, the United Arab Emirates, Qatar, and the Saudis need oil above $63 a barrel to maintain their financial health, yet oil is barely over $60 a barrel now.

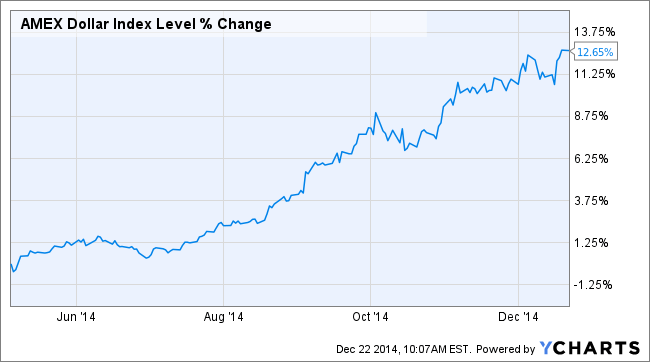

As global economies start to sputter, investor faith has faltered, as seen by the flight of cash away from global currencies into the U.S. dollar. In recent months, the value of the dollar has jumped nearly 13%, which strengthens the buying power of Americans but hurts the finances of most of the rest of the world.

To keep their currencies from losing even more value, central banks around the world are now in the unenviable position of having to raise interest rates even as their economies crave rate cuts to boost growth.

The U.S. Federal Reserve is the one big exception.

While Fed chair Janet Yellen has denied that global economic worries are influencing the Fed's decisions on setting U.S. interest rate policy, the consensus on Wall Street is that they clearly are a factor.

Last week, just before the Santa Claus rally ignited, the Fed's Federal Open Market Committee (FOMC) announced — as expected — that it would keep short-term rates near zero. The committee, however, threw Wall Street a curve ball when explaining its decision. For months, the Fed said that it expected that rates could stay near zero for "a considerable time." Investors were bracing for that language to be removed from its December press release since the U.S. economy was starting to get into gear.

As it turned out, "the phrase 'considerable time' was not dropped from the latest FOMC statement as was widely expected. Instead, it was reinforced with a new phrase stressing that the Fed can afford to be 'patient' before starting to raise interest rates," said Ed Yardeni, president of Yardeni Research.

In so doing, "the Fed didn’t remove the punch bowl; they spiked the punch," says Sam Stovall, U.S. equity strategist for S&P Capital IQ. "Akin to lighting the tree at Rockefeller Center, this response to the Fed’s actions may have signaled the start of the Santa Claus rally."

Why did the Fed cling to this "patient" sentiment?

Because the global slowdown allowed it to.

The U.S. economy is clearly gaining momentum, as Tuesday morning's GDP report clearly showed. But cheap oil caused in part by a global slowdown means that consumer prices in the U.S. should be stable. That means even as GDP is rising at a brisk pace, the Fed can keep stimulating the economy with low interest rates without fear of inflation.

In other words, what's bad for the world is good for the U.S.

Merry Christmas.