33 Smart Ways to Cut Your Taxes Right Now

- What the Democrats Winning Georgia Means for Your Wallet

- The Deadline for Retirees to Return Unwanted RMDs Is Almost Here

- How a 27-Year-Old Math Whiz (and His Uber Driver) Found a Big Flaw in an IRS Tax Formula

- Senate Tax Bill Expands the Break for High Medical Costs

- An Important Tax Deduction for Seniors and Their Families Is on the Chopping Block

- Traditional vs. Roth IRA: New Rules Could Affect How You Save for Retirement

- 5 Moves to Make Now to Lower Your Tax Bill

- This Last-Minute Tax Move Could Save You Thousands. Here's How to Do It

- An Important Retirement Account Deadline Is Coming Up. Here's What To Know

- There's a Big Tax Deadline Coming Up. Here's What You Need to Know

- Working From Anywhere? These Tips Will Help You Avoid Tax Nightmares

- If You’re Unemployed, Working From a New State or Freelancing Due to the Pandemic, Start Preparing Your Taxes Now

- Here’s How Much the Patriots Could Owe in Taxes for Their Superbowl Win

- It's Easy to File Your Taxes Online for Free in 2019. Here's How

- How You Can File Taxes Online at the Last Minute—for Free

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Preparing your 2016 tax return may feel a lot like filing last year’s did, because there are very few changes in the rules. But you’re completing this annual chore against a backdrop of uncertainty, as President Donald Trump and congressional Republicans contemplate a sweeping overhaul of U.S. tax laws.

How to proceed? Keep an eye on the doings in Washington, of course. (See a list of the most likely changes ahead.) But as you prepare for the tax deadline (which is April 18, not April 15, this year) focus first and foremost on what you can do today to trim your tax bill for 2016. “There are still plenty of last-minute moves people can make,” says Lisa Greene-Lewis, a CPA with TurboTax. And get a head start on 2017 planning while you’re at it.

The key is to home in on the special breaks for people in your particular situation—whether you are, say, building a nest egg or paying for college or celebrating a joyous event like a marriage or birth. The 33 moves that follow, organized for people in various circumstances and life stages, will help you keep more money in your pocket and away from your state and Uncle Sam.

If You Have Taxable Investments …

The stock market ended 2016 with a “Trump rally,” pushing the S&P 500 to a 12% gain—in its eighth profitable year in a row. The downside of a long bull market: the sizable capital gains tax you are likely to owe if you or the funds you own sold winners.

FOR YOUR 2016 RETURN

- Use your leftover losses. If you have investment losses from 2015 or earlier that you didn’t use to offset income on previous returns, put them to work now. Those losses can be subtracted from profits on holdings you sold in 2016 without any limit. And if losses exceed 2016 gains, you can subtract up to $3,000 of them from your ordinary income (an $840 savings in the 28% bracket).

- Report less income to your state. Most states don’t tax your funds’ income from Treasury securities. But if you own diversified taxable-bond funds, you may need to hunt around on fund-company websites for tax documents that list the proportion of Treasury interest. (For instance, in 2016, Vanguard Total Bond Market Index Fund received 30% of income from U.S. debt.) Similarly, you generally don’t have to pay state tax on income that a national municipal bond fund earned from muni bonds in your state.

PLANNING AHEAD FOR 2017

- Sell losers whenever you can. Many taxpayers wait until late in the year to check for holdings that have lost money since purchase and could be sold to offset gains. Instead, “look for opportunities to harvest ‘tax losses’ throughout the year,” says St. Louis CPA Mike Piper. An opportunity that presents itself around Valentine’s Day could be gone long before Thanksgiving. Last year, Money 50 fund iShares North American Natural Resources declined 11% in the first six weeks of 2016 before skyrocketing as global growth fears abated. You can shift into a fund that is similar, but not nearly identical, to maintain that exposure.

- Grab a 0% tax rate on gains. People in the 10% and 15% brackets (including joint filers with less than $75,900 in income and singles under $37,950) pay no tax on long-term capital gains. If that’s you, be ready to sell some winning funds later in the year, even if you will buy them back right away. Yes, you may have to pay a trading fee. But you will reset your “cost basis” (what you paid) higher, so that you’ll owe less tax on future gains than you would have otherwise. Just keep an eye on Washington: This opportunity would disappear under a plan from House Republicans.

- Put your funds in the right spots. Use your brokerage account to hold funds that won’t throw off a lot of taxable income, such as a municipal-bond fund or a low-turnover stock index fund you expect to hold for years. Stash a high-income choice like a junk-bond fund in an IRA or 401(k) to keep that income off the return you’ll file next spring.

If Your Career Has Advanced or Stalled ….

If your career saw a big shake-up last year, there’s a good chance your tax situation did too. A move up the ladder may have pushed you into a higher tax bracket. A drop in income because you were out of work may qualify you for additional tax savings. Note, though, that unemployment benefits are taxable.

FOR YOUR 2016 RETURN

- Reclaim a Social Security overpayment. If you changed jobs last year and made more than $118,500 between them, you overpaid Social Security tax, says Gil Charney, director of the Tax Institute at H&R Block. Employees were assessed 6.2% on pay up to that amount last year, but a new employer starts the counter at zero regardless of how much you already earned. Document the overpayment on line 71 on your 1040.

- Get credit for a rough spell. People who earned some income during the year but were out of work for a long time may be eligible for the Earned Income Tax Credit. Married couples with three or more kids can have an income of $53,505 and still qualify to lop up to $6,269 off their tax bill.

- Deduct job-change costs. If 2016 job-hunting expenses like printing, résumé preparation, and travel—plus other miscellaneous expenses—added up to more than 2% of your income, the amount over that can be deducted if you itemize. That 2% floor will be lower than usual in dollar terms if you had a tough year. One caveat: You must be looking for a job in your current field. Separately, if you had to relocate to land a new job, you might be able to deduct unreimbursed moving bills.

- Save on any schooling. Did you take courses at a college or vocational school to help you advance? The Lifetime Learning Credit can trim your tax bill by up to $2,000 if your income didn’t exceed $65,000 for a single filer or $131,000 if married and filing jointly.

PLANNING AHEAD FOR 2017

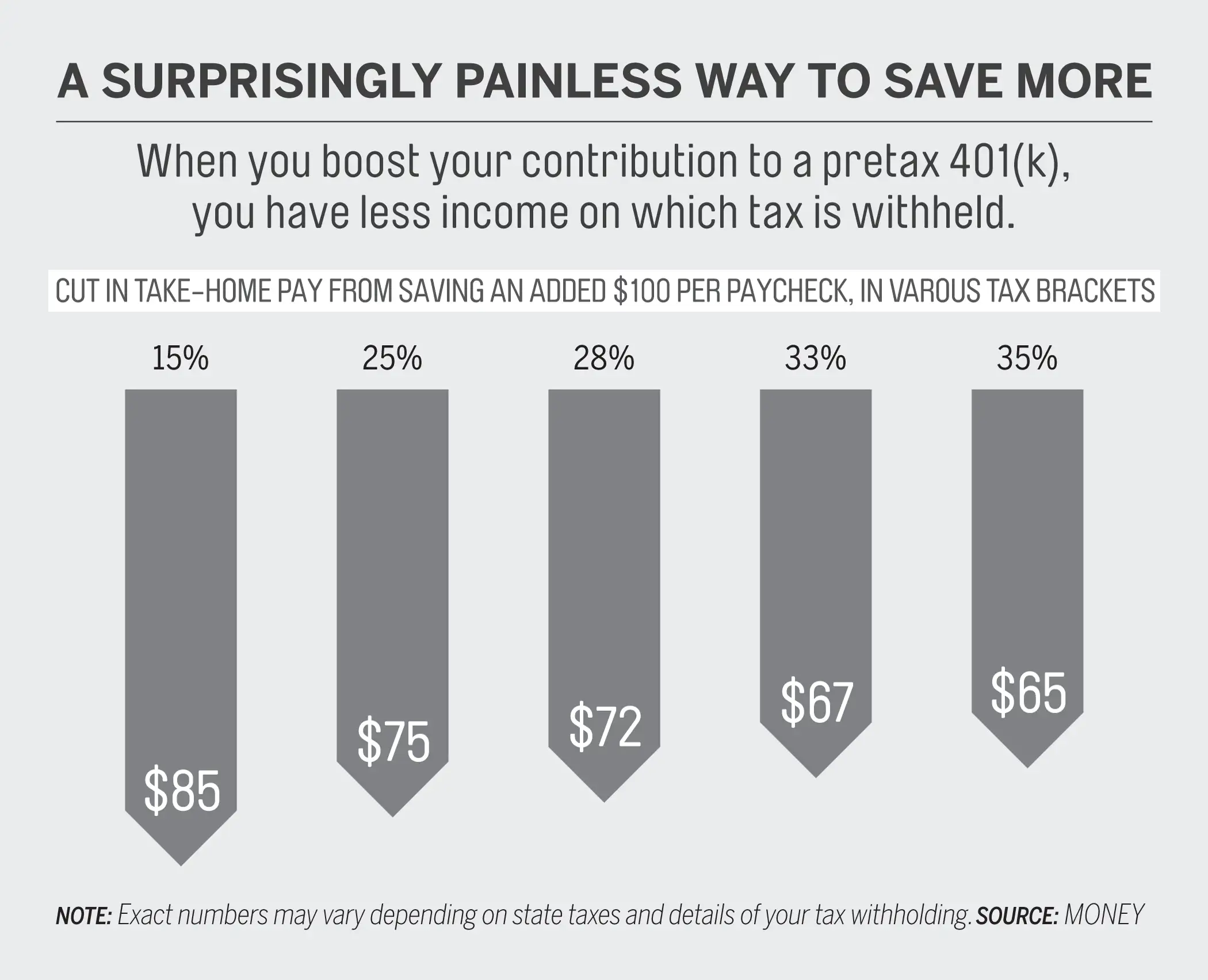

- Save your raise. Before you get used to the higher take-home pay of a fab new job, boost your 401(k) contribution. If it’s a traditional plan funded with pretax dollars, you’ll lower your tax bill for 2017. The annual maximum you can set aside from your pay remains at $18,000 if you are younger than 50, plus another $6,000 if you are at least 50 or will celebrate that birthday by year-end. (Your take-home pay may go down by less than you feared, as you can see in the graphic below.)

- Be careful with 401(k) rollovers. If you’ve changed jobs, you may decide to shift money from your old company’s 401(k) to an IRA or your new employer’s plan. The IRS last year eased the rules for people who take money from one plan and err by having it in their hands for more than 60 days on the way to the next spot. It’s now easier to avoid having the full amount taxed—along with a 10% penalty—when that happens. Still, there’s no reason to take the risk. Make sure you do a direct institution-to-institution transfer, says Michael Sonnenblick, editor and author with Thomson Reuters Tax & Accounting.

If You're New to the Working World…

Last year’s college graduates entered a job market with the lowest unemployment rate since 2007 and with more than 40% of employers expecting to ramp up hiring, according to a survey from the National Association of Colleges and Employers.

If you’re a young adult who has just joined the full-time workforce, you may have more taxable income than you have ever had before, although you also become eligible for more tax breaks.

FOR YOUR 2016 RETURN

- Deduct some student loan interest. Just started repaying student loans? You can deduct up to $2,500 in interest you paid in 2016 if the loans are in your name, you can’t be claimed as a dependent, and your income didn’t exceed $80,000 as a single filer. It’s an “above the line” deduction, meaning you can take it even if you don’t itemize.

- Choose a Roth IRA instead of a standard IRA. You can still contribute to an IRA for 2016 and deduct the contribution on your return. But if you haven’t invested yet, a better route is to go with a Roth IRA instead, says Craig Wild, a CPA in Woodbury, N.Y. This is one situation in which it may be better to forgo a tax break now for a richer one down the road. A tax deduction isn’t worth a lot when you are in a low bracket. With a Roth, you give up that tax break to instead pay no tax on withdrawals later on, when you are likely to be in a higher bracket.

PLANNING AHEAD FOR 2017

- Account for your side-gig income. The W-4 form you filled out for your employer sets your tax withholding so that you ideally don’t get a huge refund or a steep bill when you file. But you could be in for a painful surprise if you also have substantial outside income from which tax isn’t withheld, such as from a side job driving for Uber or selling crafts on Etsy. Fill out a new W-4 specifying an additional amount to be withheld from your regular pay so you won’t get hit with a big bill in April 2018, says Greene-Lewis of TurboTax.

If You Have Obamacare Coverage …

About 85% of people who bought 2016 health coverage through Affordable Care Act marketplaces got a price break: a subsidy paid by the U.S. to their insurer. But if you earned more in 2016 than the estimate you gave when you signed up, you may owe back some of that aid. Last year, some 60% of subsidy recipients who filed their taxes with H&R Block had to pay back an average $716, the firm says.

FOR YOUR 2016 RETURN

- Grab a last chance to trim 2016 coverage costs. Compare your actual 2016 income with what you had estimated (check on healthcare.gov if you bought there). You can still lower your income retroactively by contributing to your IRA or health savings account by April 18. (Use this guide for help.) To figure exactly how much to put in, use IRS Form 8962.

PLANNING AHEAD FOR 2017

- Avoid a painful surprise if your income rises. If you signed up for Obamacare for 2017, be ready to boost retirement contributions if your pay grows vs. the estimate. You can also tell the marketplace that you want to take less than the full premium subsidy that you’re allowed based on your estimated income. Yes, you’ll pay more now, but you’ll get it back next tax season if your income matches your estimate.

If You're Saving or Paying for College ...

Thirty-two states plus the District of Columbia offer a tax break for people saving for college, while there are two U.S. credits and one deduction, with varying rules, for people who paid tuition in 2016. One big change for 2017 returns: The $4,000 tuition and fees deduction used by an estimated 1.7 million families has expired. It’s still possible that Congress will restore that program, as it has done before.

FOR YOUR 2016 RETURN

- Nab a last-minute 529 break. Residents of seven states can still make a contribution to a state-sponsored 529 college savings plan that will earn a deduction for 2016 state tax returns, says Kathryn Flynn, content director at Savingforcollege.com. In Mississippi and Oklahoma, married couples can deduct up to $20,000. The five other states are Georgia, Iowa, Oregon, South Carolina, and Wisconsin.

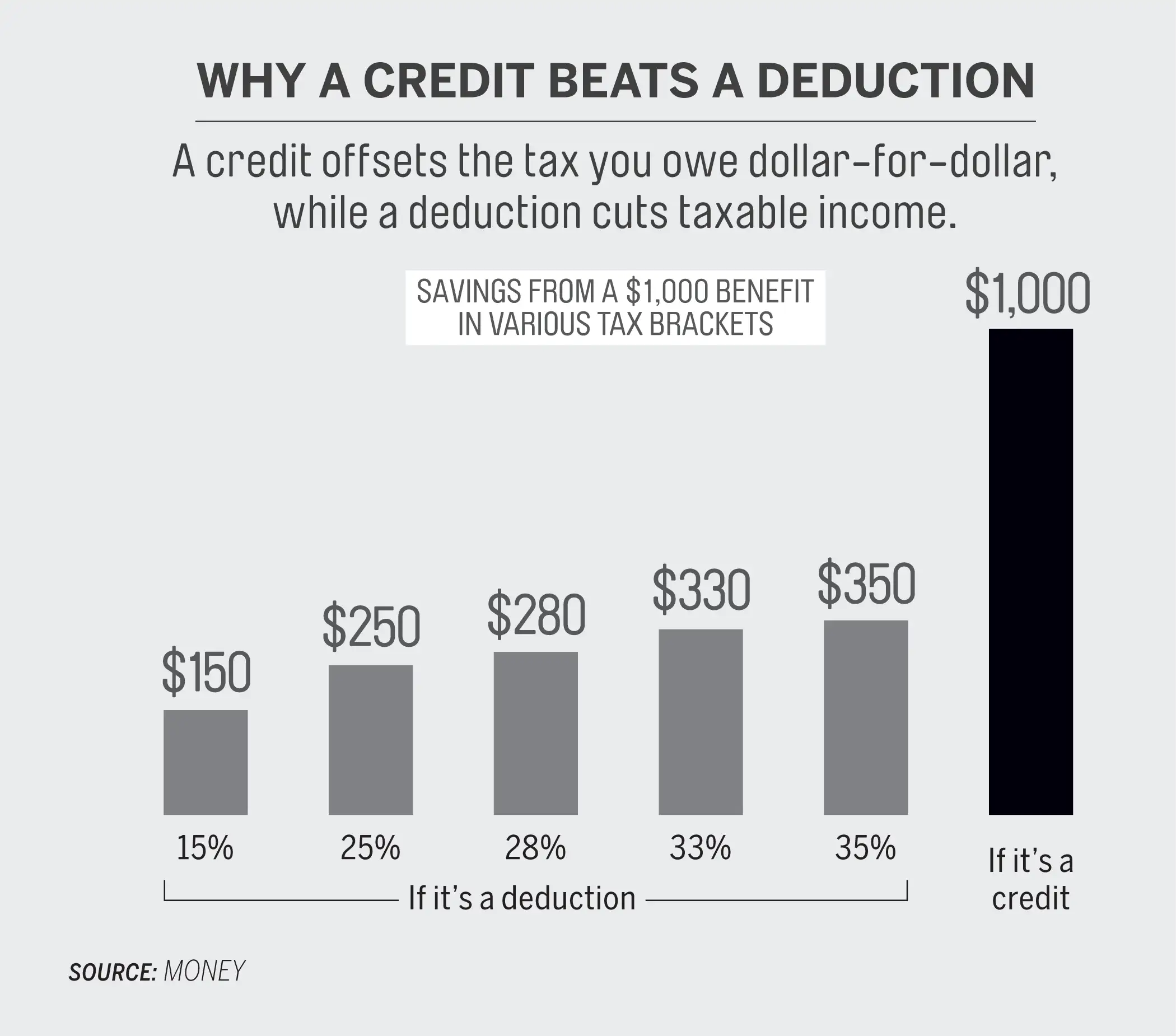

- Seize the American Opportunity Tax Credit. For parents currently paying college bills, the AOTC is a richer break than the Lifetime Learning Credit or the tuition deduction (and you can use only one). “If you can claim it, the AOTC is the best of the bunch,” says Chris Wittich, a CPA in Minneapolis. You can cut your tax bill by $2,500 if you spent $4,000 on tuition and fees. Only the first four years of undergraduate study qualify, and you must earn below $90,000 as a single filer or $180,000 if married and filing jointly.

PLANNING AHEAD FOR 2017

- To get all the tax credit you deserve, keep receipts. If your student owes little tuition—say, she is attending a state school and receiving a generous scholarship—keep receipts for required educational materials such as textbooks and lab equipment that also count toward the Opportunity credit. In the same vein, tap a 529 account for housing expenses but not for tuition, since you can’t count spending from a 529 toward the credit.

If Your Life Has Changed in a Big Way …

Marriage, the birth of a child, divorce, the death of a spouse. A significant joy or sorrow in your family could mean a sizable impact on your taxes as well. If so, file a new W-4 form with your employer to adjust your withholding, if you haven’t done that already. Your filing status for 2016 (here's the IRS guide) is based on your situation at year-end, with one key exception.

FOR YOUR 2016 RETURN

- Newlyweds: File a joint return. “A lot of people believe that it is better to file as married [filing] separately,” says Troy Lewis, a CPA in Draper, Utah. But contrary to what they think, filing separately doesn’t help you avoid the so-called marriage penalty, or tax increase that many couples with similar earnings face after they are wed. You’ll do better filing jointly except in rare situations, such as if one of you has low pay but high miscellaneous expenses, which are deductible only above 2% of income.

- Take credit for that beautiful new baby. You get to claim a child tax credit of up to $1,000 per child, in addition to an exemption for that new family member. Married couples filing jointly can claim the full credit up to $110,000 of income. It is phased out above that; for a couple with one child, a reduced credit is available for incomes below $130,000. One requirement: You must have a Social Security number or taxpayer identification number for your little one.

- After a divorce, become head of household. An unmarried custodial parent will typically qualify to save money by filing as a “head of household.” If you have $55,000 of taxable income, for instance, you’ll cut your tax bill by $1,474 (to a total $8,048), compared with filing as “single.” You can do this even if your ex claims the exemption for your child.

- Deduct any alimony you pay. You can deduct alimony checks you write to your ex, while he or she must report it as income. (Child support, by contrast, doesn’t get deducted or taxed.) You and your ex should make sure alimony sums match on your tax forms; otherwise you could be hearing from the IRS, says CPA Gail Rosen of Martinsville, N.J.

- Widow or widower? File jointly one last time. This is a rare case in which your tax status isn’t determined by where you stand on Dec. 31, says Rosen: No matter how few days of 2016 your partner saw, you can still submit this year’s return as married filing jointly, a better outcome financially than filing as single or head of household.

PLANNING AHEAD FOR 2017

- Fund an IRA for a nonworking spouse. Couples filing jointly can contribute up to $5,500 from one spouse’s income to a spousal IRA for the other. (It’s $6,500 if the account owner is 50 or older at year-end.) Depending on your income and if you have a retirement plan at work, you may be able to deduct your full contribution. For a 40-year-old in the 28% tax bracket, that could save $1,540.

- Double up on childcare breaks. For higher-earning parents, the most valuable childcare benefit is usually a dependent-care flexible spending account at work. But if you signed up to have the maximum $5,000 set aside from your pretax pay and you have expenses above that, apply the excess toward the child and dependent care credit on your 2017 return. Working parents can collect between 20% and 35% of qualifying expenses, up to maximum bills of $3,000 for one child or $6,000 for two or more.

- Cut a deal with your ex. After a divorce, a custodial parent with low pay can allow a higher-earning ex to claim their child as a dependent—generally required to get the child tax credit and any education expense credits—in exchange for a lump-sum payment.

- Widowed parent? Claim special status. If you have a dependent child and don’t remarry, you can file for the next two years as a “qualifying widow or widower,” retaining the same benefits as married filing jointly.

If You're Retired ...

Taxes can erode a big portion of your income in retirement, especially when you begin tapping your pretax retirement accounts. The required minimum distributions (RMDs) starting at age 70 1⁄2 can push you into a higher tax bracket.

FOR YOUR 2016 RETURN

- Keep pumping up your savings. Got some income from a part-time job or consulting for your old employer? If you are under 70 1⁄2, you can still lower your 2016 tax bill by stashing up to $6,500 in a pretax IRA by the tax-filing deadline. (That beats the $5,500 cap for people under 50.) If you have self-employment income, such as consulting pay, you could alternatively fund a SEP-IRA with 20% of the profit left after an adjustment for self-employment tax.

- Take your last chance before deducting health costs gets tougher. This is the last return on which the threshold for deducting medical expenses is 7.5% of income for people 65 and older; it rises to 10% (already the rule for younger filers) for 2017. If you have $80,000 in adjusted gross income, the threshold is $6,000 rising to $8,000. Don’t forget that you can deduct what you pay for insurance, including Medicare Part B doctor coverage, Part D drug coverage, and a Medigap supplement policy, which together could add up to more than $4,500 per person. If you are paying for a long-term-care policy that meets certain requirements, you can include up to $3,900 of that cost between ages 61 and 70, and $4,870 at older ages.

PLANNING AHEAD FOR 2017

- Opt for a Roth IRA conversion. If you are a recent retiree in a low tax bracket, take advantage by converting some of the money in pretax 401(k)s and IRAs to a Roth. You will owe tax on what you convert, but if you are in a higher bracket in the future, you are likely to come out ahead. Of course, estimating your future bracket is dicey, given Washington’s plans to change taxes. But it’s not risky to go ahead, since you can undo a 2017 Roth conversion as late as mid-October 2018. “It’s about the only tax do-over you can get,” says CPA Jeffrey Levine of Ed Slott & Co. Do this only if you can pay taxes with money outside your IRA, so that you don’t dilute the nest egg that will keep growing tax-free in the Roth.

- Not itemizing? Grab a charitable benefit. If you’re over 701⁄2, you can make charitable gifts of up to $100,000 a year via a direct donation from your IRA. This may be especially valuable to you if you don’t itemize deductions and thus don’t usually get any write-off for giving. The transfers count toward your RMDs and aren’t taxed as those distributions ordinarily would be. (This move can also be attractive for some itemizers, but you lose the charitable donation.)

- Fund a grandkid's 529 plan. You can get a state tax deduction in many states for putting money in a 529 college savings account for a grandchild. And there’s also an option to superfund a 529—by bundling five years of gifts into one year—that may appeal to some well-off seniors who are concerned about estate tax. You can contribute $70,000 per grandchild (or $140,000 for married couples) without having to file any special IRS paperwork or face potential gift and estate tax.