Investors have been suffering from a case of whiplash. Late last year, the stock market, having posted one of the worst Decembers in decades, seemed to be flirting with bear market territory. Then suddenly the picture brightened. The Fed, which had been gradually hiking interest rates, relented. Meanwhile, U.S. corporate profits a major driver of U.S. growth, began to look healthier than they had just a few months before. By April, the S&P 500 had set a new record high.

Crisis averted? Not so fast. Remember that while the stock market loved the Fed’s rate-hike pause, it’s a sign policymakers see growth slowing, not speeding up. What’s more, even amid the rally, trade tensions with China reemerged and the bond market began giving off bearish signals, all of which suggest the underlying tensions behind December’s swoon haven’t resolved, only moved to the background. The same tug-of-war between market forces is likely to drive your investment returns for the rest of the year—and into 2020. Here is what you need to know.

1. Rates Hold Steady

Two big things impact stock prices: “The cost of money and earnings,” says Ernie Cecilia, chief investment officer of Bryn Mawr Trust in Berwyn, Pa. While the U.S. government can do only so much to boost corporate earnings, it plays no small role in controlling the cost of money by setting targets for the Federal funds rate—what banks pay for short-term loans to one another.

A slight change in this rate may seem innocuous, but even that can send the stock market into a frenzy. Not only do Fed rates have a ripple effect throughout the economy—such as by making corporate debt or home loans cheaper or more expensive—they also change the relative appeal of stocks vs. bonds. When rates are low, as they have been, investors seek higher returns in riskier assets like stocks.

This is all to say that when the Federal Reserve unexpectedly pushed the pause button on its plans to gradually increase its target rate, it was a big deal. “Investors weren’t expecting this,” says Adrian Helfert, director of multi-asset portfolios at Westwood, a Dallas-based investment and asset management firm. “This is one of the reasons we saw stocks rally in the first quarter.”

Following the financial crisis, the Fed dropped its target rate to close to zero and held it there until 2015. Policymakers had been gradually bringing that up to the current target of 2.25% to 2.5% and were on track to raise that to 3% by the end of 2019. Then, following weaker-than-expected economic data—not to mention the nearly 20% stock market plunge in the fourth quarter—the Fed had a change of heart. The first hint of a pause came at the end of January, and on March 20, Federal Reserve Chairman Jerome Powell reaffirmed that view, saying rate hikes could be on hold for “some time.”

All things being equal, lower borrowing costs are good news for the stock market—at least in the short term. There is also the potential that this time-out could create a virtuous cycle by nudging consumers to spend a little more and companies to invest in productivity-boosting capital, ultimately improving real earnings growth. Although two-thirds of CFOs surveyed for Duke University’s Global Business Outlook predict a recession by the third quarter of 2020, they also expect capital spending and revenue to increase by 5% over the next 12 months. In keeping rates in check, “the central bank gave an extraordinary handshake to CFOs and investors and said, ‘We will be there for you,’ ” Helfert notes.

CAVEAT

As much as investors love this rally, many worry—and rightly so—that Fed stimulus at this stage might be the economic equivalent of pounding espresso shots at 2 a.m. “This economic expansion is almost 10 years old, and though monetary policy is neutral, there aren’t a lot of levers left to fuel further growth in the economy,” says Cecilia. It’s possible that this pause could give a new gear to growth, but it may just be delaying the inevitable.

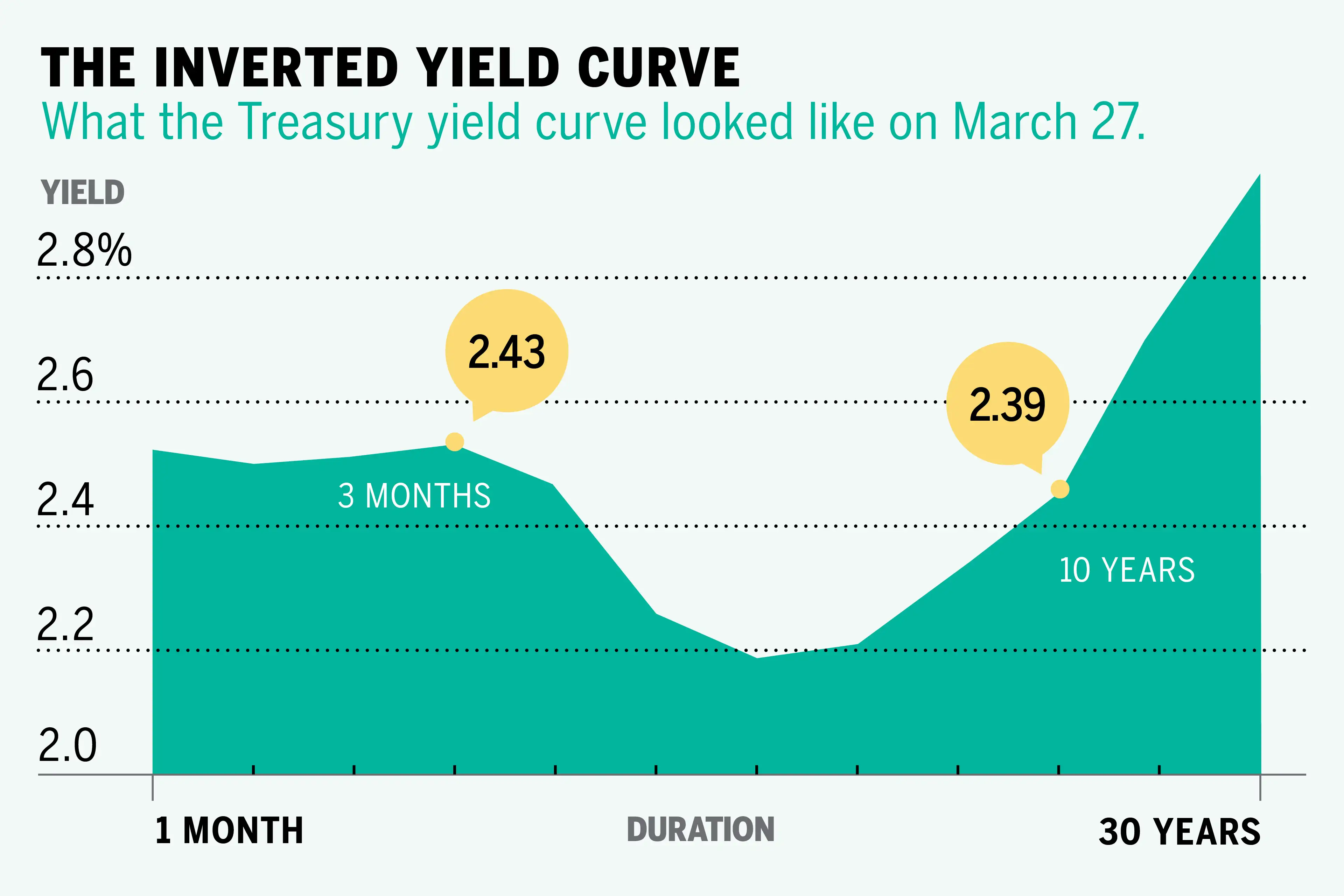

2. The Curve Swerves

In late March, bond market investors witnessed something they had been waiting for—and dreading—for months. The event, known as a “yield-curve inversion,” took place when yields on short-dated three-month Treasury bills slipped above those of much longer 10-year bonds. While that may seem like a statistical oddity, to bond investors it’s a notorious omen. A recent Federal Reserve study noted a yield-curve inversion preceded each of the past seven recessions by roughly a year. The last time short-term yields eclipsed longer-term ones was in August 2006, roughly 15 months before the onset of the financial crisis.

It’s not hard to understand why the situation is unusual. Bond investors are essentially lenders, and they demand higher interest rates for longer-term loans since risks—like a jump in inflation or interest rates—are greater. Plotted on a graph, these progressively higher rates make an upward-sloping curve—the yield curve. Ahead of a recession, however, the calculus can change. Expecting the Federal Reserve to cut interest rates to boost the pace of growth, bond investors scramble to purchase longer-dated bonds and lock in today’s higher rates for as long as possible. The demand pushes long-term yields downward, sometimes even below short-term yields, reversing or “inverting” the slope of the yield curve.

CAVEAT

While every recession in recent history has been preceded by a yield-curve inversion, not every inversion has been followed by a recession. Federal Reserve researchers noted at least two “false positives,” in 1966 and 1998, that were not followed by a recession. What’s more, while the yield curve often inverts for weeks or months before economic growth begins to slow, March’s inversion proved vanishingly brief—lasting just five days.

Even if you expect a recession in the coming months, that doesn’t mean you should panic and sell all your stocks. A recent study of past yield-curve inversions by investment firm LPL found that the stock market continued to rise for anywhere from eight months to nearly two years afterward. During those periods, investors frequently reaped double-digit gains.

3. Profits Snap Back

One big reason stocks took a hit last winter: weaker-than-expected corporate earnings. In fact, for the fourth quarter a whopping 25% of companies reported profits that were lower than analysts expected—the highest percentage in any three-month period since 2013.

The good news is that since then, a number of things have changed to boost profits, namely the Fed’s rate-hike pause, which made it easier for companies to borrow, and strong U.S. consumer confidence and spending. Less than 20% of companies missed analysts’ targets the first quarter.

Investors pay such close attention to company profits because they go hand in hand with economic growth, translating into investment in new equipment and jobs for workers—in addition to funding dividends and buybacks that more directly boost share prices.

In general, earnings are expected to remain strong as the economy continues to grow, although not as quickly as some investors had hoped last year, according to Howard Silverblatt, senior index analyst at S&P Dow Jones Indices. Home prices and consumer confidence—two major growth drivers—continue to rise. With the Federal Reserve’s recent decision to refrain from boosting interest rates, borrowing costs for most businesses should remain manageable. S&P 500 companies on average earned $152 per share in 2018, according to S&P Dow Jones Indices. Wall Street analysts expect earnings to grow 9%, to $166 per share, in 2019—and another 12%, to $185 per share, in 2020, on average.

CAVEAT

Last year corporate profits jumped as much as 20%, after the Tax Cuts and Jobs Act cut the corporate tax rate to 21% from 35%. While companies will continue to enjoy the new, lower rate, the dramatic jump in earnings—which helped propel stock prices upward—won’t be repeated. Rising wages for U.S. workers and slowing economic growth in Europe and Asia could pose additional risks. On average, S&P 500 companies on the whole get nearly 44% of their sales from abroad. For the important tech sector, it’s even higher—nearly 60%.

4. Tech’s Bull Keeps Charging

Tech stocks have been the driving force behind the stock market’s big gains in recent years. Still, many experts think these stocks—particularly the so-called FAANGs—can continue to pull their weight.

FAANG stands for Facebook, Amazon, Apple, Netflix, and Google. The giant valuations of these high-flying tech stocks mean they make up a disproportionate share of the market and drive a disproportionate share of its gains. Just how big is their influence? While the S&P 500 gained 9.4% over the 12 months ended March 31, without these stocks, it would have gained just 7.5%, according to Morningstar.

In other words, even if you merely invest in funds that mirror the broad market, these stocks can have an outsize effect on your returns. The good news is many experts remain bullish. Google, for example, is still the king of search, with the majority of its revenue coming from advertising. But the company is also expanding into other businesses, like self-driving-car startup Waymo and health care venture Verily. Although some of these projects have yet to generate revenue, they could tap into markets worth tens of billions of dollars within the next 10 to 15 years, according to Morningstar.

Streaming-entertainment company Netflix, which has nearly 140 million global subscribers, is expected to surpass 200 million in the next few years, according to several estimates. Those extra subscribers should help the company double the amount it earns from streaming by 2020—to $11 billion from $5.6 billion, according to brokerage Raymond James.

CAVEAT

Many FAANG stocks aren’t cheap. Netflix and Amazon have high price-to--earnings ratios of 136 and 97, respectively. That means there is little room for error if the growth investors expect doesn’t materialize.

While Apple, trading at 18 times earnings, is cheaper, in many ways, it’s a case in point. While the iPhone transformed computing and made Apple for a time the most valuable company in the world, sales have stalled, and the company has yet to come up with a new blockbuster. During the fourth quarter, iPhone sales amounted to 65 million—down from 73 million at the end of 2010. “Apple is in for a long transition from being hardware dependent to becoming more of a services company—and it could take years for that to kick in,” says Mark Baribeau, head of global equity at Jennison Associates.

5. China Weathers the Trade Storm

The world’s second-largest economy has been a global workhorse, posting average GDP growth of about 10% since the late 1970s. And its influence grows ever more meaningful as China’s share of the eco-nomic pie has increased. China has accounted for a full third of global growth since 2011, according to BlackRock. Meanwhile, 57 companies in the S&P 500 derive more than 10% of their sales from China, according to FactSet. The list is wide-ranging, from Apple and Microsoft to Nike, McDonald’s, and Tiffany & Co.

So when China’s economic growth slumped to 6.6% in 2018—its slowest pace in nearly three decades—investors saw it as a reason to worry. The culprit: trade tensions coupled with the Chinese government’s own efforts to tighten fiscal and monetary policy.

As a result, China began late last year to take measured steps to stimulate its economy—and early numbers suggest they’re working. The country reported 6.4% first-quarter growth, slightly better than what most analysts were predicting. While new U.S. tariffs provide another headwind, "data still suggests there have been improvements in China’s economy,” says Kristina Hooper, chief global market strategist at Invesco. She points to improvements in purchasing managers’ index numbers, which is considered a leading indicator. Even after trade tensions sent Chinese stocks tumbling in May, they remain up nearly 10% in 2019.

Just as important as how much China is growing is how it’s growing. China has a tendency to overstimulate its economy and take on too much debt, but this time around, economists give policymakers props for showing restraint.

CAVEAT

Investors have long regarded financial data reported by the Chinese government and individual companies with skepticism. This should give you pause before betting too heavily on the Chinese stock market—and especially on individual stocks.

The U.S.-China trade spat could get worse before it gets better. while Trump administration slapped 25% tarrifs on $200 billion of Chinese imports in May, it could expand that to all Chinese goods later this year. The International Monetary Fund estimates that if all goods traded between the two nations were subject to tariffs, it would shave 0.8% off total global economic growth.