Money’s latest Best Colleges offers a practical analysis of more than 700 four-year colleges, focusing on affordability and student outcomes to help families make informed decisions about where to spend their tuition dollars.

Data collection and analysis for the ratings were led by Money’s rankings partner, Witlytic. Money’s editorial staff, however, is solely responsible for the final ratings decisions.

Here is the methodology behind our new 2025 rankings — first in a short version, followed by a more comprehensive one. Have questions about our methodology? Email us at college@money.com.

Table of contents:

- Best Colleges methodology, in brief

- How to read our star ratings

- Best Colleges methodology, in detail

- How we calculated college's ratings

- Why isn't my college rated?

- Limitations of Money's college ratings

Money’s Best Colleges methodology, in brief

We start with all of the four-year public and private nonprofit colleges in the country, a group that totals more than 2,400. To make our initial cut, a college had to:

- Have at least 500 undergraduate students or 150 freshmen.

- Have sufficient, reliable data to be analyzed.

- Not be in financial distress.

- Have a graduation rate that was at or above the median for its institutional category (public, private or historically black college or university), or have a high “value-added” graduation rate (in other words: score in the top 25% of graduation rates after accounting for the student body).

A total of 732 schools met the requirements in our initial cut. We ranked them on 25 factors in three categories:

Quality of education (30% of weighting), which was calculated using:

- Graduation rates (30%). We weigh both six-year and four-year graduation rates. Both are adjusted to capture students who transferred into a college as well as first-time students.

- Value-added graduation rate (30%). This is the difference between a school’s actual graduation rate and its expected rate, based on the economic and academic profile of the student body.

- Peer quality (15%). This is measured by the standardized test scores of entering freshman (5%), the average GPA of entering freshmen (5%) and the percentage of accepted students who enroll in that college, known as the “yield” rate (5%).

- Instructor access (10%). This is measured by the student-to-faculty ratio.

- Financial troubles (5%). Financial troubles are signaled by a college having low bond ratings, being labeled by the U.S. Department of Education as having financial issues or having accreditation warnings.

- Pell Grant recipient outcomes (10%). Federal Pell Grants are awarded to lower-income students. This measures the share of grant recipients a school graduates.

Affordability (40% of weighting), which was calculated using:

- Net price of a degree (30%). This is the estimated amount a typical freshman starting in 2025 will pay to earn a degree, taking into account the college’s sticker price; how much the school awards in grants and scholarships; and the average time it takes students to graduate from the school, all as reported to the U.S. Department of Education.

- Net price paid by students in different income brackets (20%). This is the net price for one year paid by students from families earning $0 to $30,000 (10%); students from families earning $30,001 to $48,000 (5%); and students from families earning $48,001 to $75,000 (5%).

- Debt (20%). This takes into account the estimated average student debt upon graduation (15%) and average amount borrowed through the federal parent PLUS loan program (5%).

- Ability to repay debt (15%). This measure includes the percentage of students who are making progress repaying their debt one year after leaving school (10%). It also includes a college’s Student Loan Default Risk Index, (5%) which is a calculation that weighs the share of students who borrow and the share of borrowers who default on their federal student loans.

- Value-added student loan repayment measures (15%). These are the school’s performance on the student loan repayment and default measures after adjusting for the economic and academic profile of the student body.

Outcomes (30% of weighting), which was calculated using:

- Earnings 10 years after college entry (25%). This measure, from the U.S. Department of Education’s College Scorecard, captures the median earnings of federal financial aid recipients at each college 10 years after the student started.

- College Scorecard employment outcomes (25%). This includes two measures for federal financial aid recipients: the share of alumni who are not working nor enrolled in graduate school one year after completing their degree (15%) and the share of alumni who are earning more than a high school graduate six years after starting (15%).

- Value-added earnings (20%). This is the College Scorecard 10-year earnings measure, after adjusting for the economic and academic profile of the student body.

- Graduates’ earnings adjusted for majors (15%). This takes a weighted average salary for each college, using program-level earnings data from the College Scorecard, and compares it with colleges that graduate students in a similar mix of majors.

- Economic mobility index (10%). We included data from Third Way that measures a college’s share of students from low- and moderate-income backgrounds as well as the cost and payoff of a degree for those students.

Finally, after scoring colleges this year, we grouped them into one of seven ratings, from 2 stars to 5 stars.

For a more detailed description of the methodology, read on.

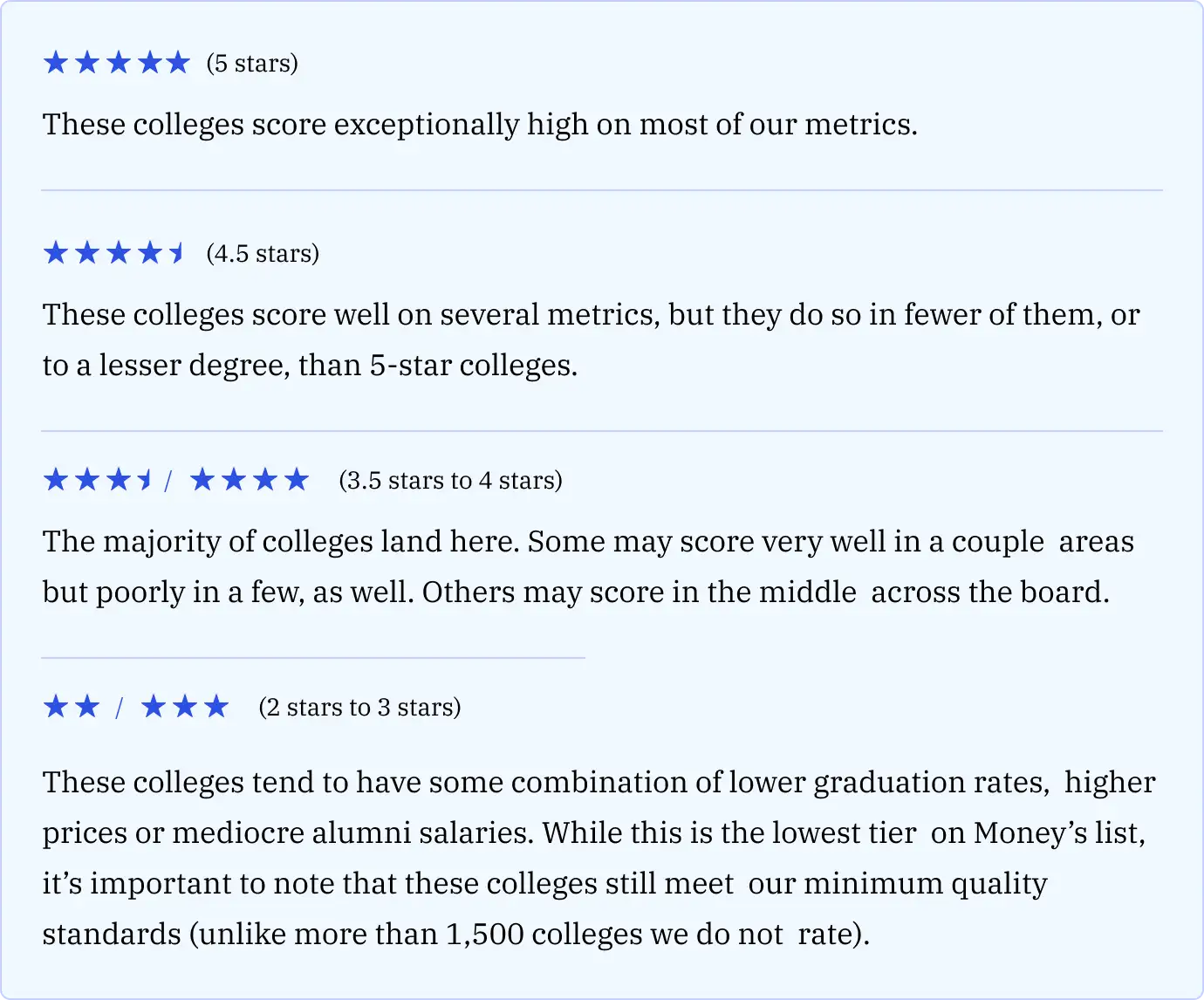

How to read our star ratings

We understand most readers are used to numerical rankings that order colleges, but we feel a rating system more accurately represents the variation in colleges’ performance. In a numbered ranking, very small differences in colleges’ scores result in different ranks, exaggerating the difference in performance. As experts have long advised, it’s more important to look broadly at where a college lands on a list and not its precise rank. (We switched to a rating system in 2022; you can read more about why we made the decision in our story from the time.)

Here's a key to help you understand the star ratings:

Money’s Best Colleges methodology, in detail

The Best Colleges ratings combine the most accurate pricing estimates available with indicators of alumni financial success, along with an analysis of how much value a college adds when compared to other schools that take in similar students.

How does Money measure a college’s “value add”

We estimate a college’s “value add” by comparing a school’s actual performance on four measures against its predicted performance, considering the students it admits and enrolls.

To gauge how well a college is performing relative to its peers, we looked at data on the admissions selectivity (as measured by standardized test scores and the average freshman GPA) and the percentage of students with incomes low enough to qualify for federal Pell Grants (the majority of which go to families with incomes below $50,000).

We then used the statistical technique of regression analysis to model the expected impact a student’s test scores, GPA and income have on key factors, such as graduation rates and future earnings. The difference between these expected values and the actual reported values represent the school’s “value add.”

Value-added measures are a way to capture some parts of a college’s quality that more commonly used metrics can’t capture. They give an indication of how a college affects graduates’ outcomes, rather than simply rewarding colleges that admit the highest-performing students.

Which colleges does Money score?

To ensure that we fairly compared apples to apples, a college must meet these criteria to be included in our universe:

- Be a public or private nonprofit college in the United States that enrolls freshmen.

- Have at least 500 in-person undergraduate students or at least 150 full-time, first-time (FTFT) students to ensure there are enough students in the graduation rate cohort to have reliable data.

- Charge tuition in dollars. We screened out military academies that require a commitment of service in exchange for free tuition because we don’t know how to value the cost of the time commitment and risk.

- Have sufficient data to be analyzed. Any college missing graduation rates or historical data needed for our value-added model was removed from our universe, and any college missing more than 5 metrics was removed from the final ranking.

- Not show signs of financial distress, as defined by having at least two of the following indicators: Low ratings by any of the three major bond-rating agencies, warnings from accreditors, or being placed on “heightened cash management 2” by the U.S. Department of Education.

- Have a graduation rate that was at or above the median for its institutional category (public, private, or HBCU). Or have a high “value-added” graduation rate (in other words: score in the top 25% of graduation rates after accounting for the student body). For these colleges, a graduation rate of 40% was used as a cut off.

- Have a student loan Cohort Default Rate (CDR) lower than 25%.

This eliminated some colleges that may be good values, but might be facing temporary financial difficulties or may be too small for us to evaluate. But it left a robust universe of more than 730 schools.

We then used the following data and calculations in our three basic categories to create our rankings:

Quality of Education: 30% of weighting

For this factor, we combined the following eight indicators:

Graduation rates (30%): Education experts and college officials generally agree that one of the most important reflections of a college’s quality is its graduation rate. Our graduation rate calculations use bachelor’s degree-seeking students only.

- Six-year graduation rate: 20%. The most commonly cited graduation rate statistic — the percentage of freshmen that graduate within six years — is based only on first-time, full-time students, meaning it misses a large population of students at many colleges. To help address that, we also use federal data to expand that graduation rate by including the share of full-time students who transferred into a college and earned a degree within six years.

- Four-year graduation rate: 10%. While the six-year rate is most commonly cited (and many places may cite an eight-year rate), most full-time students enroll with the expectation that they will graduate on time. Plus, spending more than four years in school increases the cost of a degree through direct, immediate tuition charges, but also through the opportunity cost of missed earnings while in school. For these reasons, we also weigh the four-year graduation rate.

Value-added graduation rate (30%): Many education experts and college officials point out that the basic graduation rate number, while useful, is an insufficient indicator of a college’s value because research shows that wealthier students and students who got good grades in high school are more likely to graduate on time no matter what college they attend. In other words, elite schools, which disproportionately enroll such advantaged students, are expected to have high graduation rates. For that reason, we calculated each school’s relative performance after accounting for the economic background and academic preparation of its students (measured by the percentage of attendees receiving Pell Grants, the majority of which are given to low-income students; the standardized test scores and high school GPAs of incoming freshmen; and the share of full-time, degree-seeking students on campus). The higher a school’s graduation rate was above the rate predicted for a school with that particular mix of students, the more value that particular college is assumed to have added. We use six-year graduation rates for our value-add model.

Peer quality (15%): Decades of research have shown that undergraduates have a major impact on their peers. Our peer quality measure consists of these three indicators:

- Standardized test scores (5%): We used composite test scores of incoming freshmen to estimate the academic qualifications of the student body. While there is much debate over the usefulness and validity of standardized tests, the SAT and ACT tests currently provide the only nationally comparable data on student abilities.

- Average GPA (5%): We used the average GPA of incoming freshmen provided by Peterson's. This measure is new this year, added to diversify our peer quality measure since so many schools have transitioned to test optional admissions policies.

- Yield (5%): The federally reported “yield” is the percentage of accepted students who enroll in a given college. The higher the yield, the more likely it is that the school was the student’s first choice, or best option, and that applicants perceive the college’s quality as high.

Faculty (10%): Research shows that students who get more individual attention from faculty tend to achieve more, both in college and after graduation. (See, for example, this Gallup-Strada study.) We include each school’s student-to-faculty ratio.

Financial troubles (5%): Financial difficulties can affect the quality of education, through layoffs of staff, closure of academic programs and reduction of services. A school was deemed to be facing financial trouble if it:

- Is on the “Heightened Cash Monitoring 2” list published by the U.S. Department of Education, reflecting concerns about the school’s financial stability.

- Has bonds that are rated below-investment grade by Standard & Poor’s, Moody’s or Fitch.

- Has received warnings from its accreditor.

Pell Grant recipient outcomes (10%): To analyze how well schools help low-income students succeed, we multiplied the share of federal Pell Grant recipients on campus with the six-year graduation rate for Pell grant recipients in the school’s bachelor’s degree-seeking cohort. Schools that serve a large share of low-income students and help them graduate rise to the top.

Affordability: 40% of weighting

For this factor we used 10 indicators, weighted as shown:

Net price of a degree (30%): Money uses a unique estimate of college prices. We started with the “sticker” price provided by the college to the federal government. The full cost of attendance includes tuition, fees, room, board, books, travel and miscellaneous costs. (In calculating tuition and fees for public colleges, in-state amounts were used.)

We then subtracted the average amount of institutional aid provided per student by the college. That gave us an estimate of the net price the college charged an average student for the most recent academic year these data were available.

Next, we used federal data on the percentage of students who graduate from that college in four, five and six years to factor in how long a typical student is enrolled before earning a degree. We generated an estimated net price for a series of six years, inflating each slightly since tuition prices typically rise each year. We then created a weighted average total net price, based on those prices and the proportion of students who complete their degrees within four years, five years and six years. A handful of exceptions are made for institutions with longstanding co-op programs, as those programs intentionally extend the length of a degree and no tuition is charged during co-op periods.

The federal net price estimate for a year’s costs is typically lower than Money’s estimate because the Department of Education subtracts almost all grants — federal, state and institutional — while we only subtract aid provided by the school, for reasons described in the ‘limitations’ section below.

Money gives the net price sub-factor a very heavy weighting because surveys consistently show that the cost of college is one of families’ biggest worries.

Net price by income bracket (20%): The federal government reports the annual average price paid at each school by federal aid recipients broken down into five income groups. Given the way college costs have outpaced income growth in the last few decades, even many middle-income families report that paying for college is out of reach. As a result, we look at three income brackets to capture affordability for low- and middle-income families. We award the most weight to the lowest income group as an indicator of how well the college targets need-based financial aid:

- Net price for students from families earning $0-$30,000 (10%)

- Net price for students from families earning $30-001-$48,000 (5%)

- Net price for students from families earning $48,001-$75,000 (5%)

Educational debt (20%): Surveys show unaffordable debt to be another of students’ biggest worries about attending college, and research shows student debt can have long-lasting effects on young adults’ finances.

Our educational debt assessment is based on these two indicators:

- Student borrowing (15%): Our measure of student borrowing starts with the average dollar value of federal student loans by entering undergraduates, multiplies that by the share of entering undergraduates that take out a federal student loan, then multiplies that again by the institution’s average time to degree. This generates the average total federal student loan amount across all entering undergraduate students. These data are reported by the federal government or calculated using federally reported data. A handful of exceptions are made for institutions with longstanding co-op programs. We capped the dollar value of student loans at $9,500, the federal maximum for first-year students who are considered independent according to the government’s financial aid rules.

- Parent borrowing (5%): The federal government reports the total amount of parent PLUS loans awarded to parents at each college each year. We divided this number by the school’s total undergraduate enrollment to calculate an average parent PLUS debt per undergraduate student. While other organizations generally don’t include parental debt in their rankings, Money believes parent educational borrowing is a financial burden and should be an important consideration.

Ability to repay (30%): The ability to repay loans taken out to finance a college education is another indication of a school’s affordability for its students. We evaluated ability to repay using these four indicators:

- Student loan default risk index (SDRI) (5%): Each year, the federal government publishes the number of former students who left college three years ago and have since defaulted on their federal student loans. Using a methodology proposed by The Institute for College Access and Success (TICAS), Money adjusts these numbers for the share of undergraduate students at the college who take out federal student loans. This is intended to indicate the odds that any particular student at the college will end up defaulting on a student loan.

- Value-added SDRI (5%): We measured whether a college’s SDRI was above or below the rates typical of schools with similar student bodies.

- Federal student loan repayment (10%): To calculate a repayment rate, we used federal College Scorecard data on both the percentage of student borrowers who are making progress paying down their loans and the percentage of students who’ve paid off their loans one year after starting repayment. In the past, we’d used a three year time period for this measure. Because the federal government hasn’t updated this data in several years, we swapped to a one year time period to include a more recent cohort of students.

- Value-added student loan repayment (10%): We measured whether a college’s student loan repayment rate was above or below the rates typical of schools with similar student bodies.

Outcomes: 30% of weighting

For our third category, we used a total of seven indicators, weighted as shown below.

Earnings 10 years after college entry (25%): These are the median earnings in 2019 and 2020 of people who started as college freshmen and received federal aid between 2008 and 2010 and are currently working and not enrolled, published in the U.S. Department of Education’s College Scorecard. Earnings are inflation adjusted up to 2021.

Value-added early career earnings (20%): We analyzed how students’ actual earnings 10 years after enrolling compared with the rate predicted of students at schools with similar student bodies.

Share of graduates who don’t have a job after one year (15%): This data from the College Scorecard shows the percentage of federal financial aid recipients who graduated in 2017-18 or 2018-19 and were neither enrolled in school nor employed a year later. Lower values are scored higher, so that colleges where a larger share of graduates are working perform better.

Share of students earning more than a high school graduate within six years of starting college (15%): The federal government publishes these data to show which colleges produce alumni who are earning at least as much as the typical high school graduate. It is based on incoming freshmen in 2012-13 or 2013-14 who received federal financial aid.

Major-adjusted early career earnings (15%): Research shows that a student’s major has a significant influence on their earning potential. To account for this, we used College Scorecard program-level earnings of students who graduated between 2015 and 2018. These are the earnings of graduates from the same academic programs at the same colleges, one and two years after they earned a degree. We then calculated an average salary, weighted by the share of the bachelor’s degree completers in each major (grouped by CIP program levels). Then, we used a clustering algorithm to group colleges that have a similar mix of majors and compared the weighted average against colleges in the same group. Colleges whose weighted average was higher than that of their group scored well. This allows us to compare schools that produce graduates who go into fields with very different earnings potentials.

Economic mobility (10%): Think tank Third Way published economic mobility data for each college, based on a college’s share of low- and moderate-income students and a college’s “Price-to-Earnings Premium” (PEP) for low-income students. The PEP measures the time it takes students to recoup their educational costs given the earnings boost they obtain by attending an institution. Low-income students were defined as those whose families make $30,000 or less. We used this as an indicator of which colleges are helping promote upward mobility.

How we calculated colleges' ratings

For each of our data points, for each college, we calculated a “Z-score” — a statistical technique that turns lots of differently scaled data into a standard set of numbers that are easily comparable. We then scored each z-score according to the weights outlined above. We capped outliers at the top and bottom of the scale in a handful of categories to limit how much a college’s score can be driven by strong (or poor) performance in a single category.

Finally, we assigned colleges into one of seven star ratings: 2, 2.5, 3, 3.5, 4, 4.5 and 5, with 5 being the highest classification. We grouped colleges according to natural clusters in their total scores. The groupings are based on standard deviations that result in a bell curve — colleges with similar scores are clustered in the middle, while there are a smaller number of higher and lower-performing colleges.

How we accounted for colleges that were missing data

We imputed SAT/ACT scores and GPAs for colleges with missing data using the average values for a college’s Carnegie classification and selectivity. For any other missing values, we assigned the average value of the remainder of this list for that specific data point.

Why isn’t my college rated?

If a college does not appear on our list that means it did not meet one of the initial screening requirements outlined above. Those requirements include enrollment cutoffs and having sufficient data to analyze. But the most common reason colleges don’t make the cut is that their six-year graduation rate is too low.

Colleges need a graduation rate that was at or above the median for its institutional category. This year, those medians were 57.85% for public colleges, 64% for private, not-for-profit colleges, and 37.05% for historically Black colleges and universities.

You may notice that some colleges with graduation rates below those cutoffs are still included. In those cases, the colleges were originally disqualified but got brought back into the universe because they had exceptionally high value-added graduation rates. That means our analysis shows their graduation rate is much higher than expected given the students who enroll. This year, nearly 100 colleges were added to the universe this way.

Limitations of Money’s college ratings

While we believe our rankings are better than any others out there, we know they are not perfect. Here are some caveats that we are aware of.

Limitations on earnings and employment data. The earnings data in the College Scorecard only captures students who received federal financial aid. At some colleges, this may capture the majority of students, if most students either borrow student loans or receive federal grants. But at some campuses, the earnings data will be based on a small portion of the students that college educates. The earnings data available is also limited to short time frames. For program-level earnings, for example, it only captures alumni within a few years of graduation. Plus, many smaller college programs are not reported due to privacy concerns. As the government continues to release more earnings data that captures more students over a longer period of time, we feel our analysis will improve.

Student learning. What students actually learn is a big unanswered question in higher education. We have not been able to find good data on basic indicators of academic rigor, such as the number of pages of writing or reading required per assignment or a national measure of how much students learn.

Standardized tests. Since 2020, colleges have made a large shift to “test-optional” policies, by giving applicants the choice of whether to submit SAT or ACT scores. Some colleges have made the switch permanently, while others are conducting multi-year experiments, and it’s unclear how many colleges will stick with the policy. Still, if this trend continues and grows to the point where a large population of students at many of the colleges in Money’s universe do not submit scores, we’ll have to evaluate the effect that has on our rankings, particularly our value-add assessments that rely heavily on scores to predict academic performance.

Geographical cost of living adjustments. Some colleges in low-wage, low-living-cost areas, such as parts of the south and midwest, may get lower scores because we have not adjusted the earnings data for the cost of living. While there are some factors in our rankings that lessen the impact of any geographic wage differential — including the College Scorecard employment data, student loan default rate, debt repayment rate — we recognize this is still a weakness. We note, though, that we also do not conduct any cost of living adjustments in our net price of a degree calculation, and colleges in the south and west often score well here.

Out-of-state public college tuition. Colleges charge higher prices to out-of-state students. Out-of-state students can still use our rankings to assess public colleges on their educational quality and alumni outcomes, but the affordability metrics — specifically net price and average borrowing levels — likely will not apply.

Net prices. Money’s estimated net price of a degree is likely to be higher than the average price actually paid by most families at that institution. It is crucial to understand that while the Money net price estimate is based on the average price charged by the college, you and your family will pay less than that if your student receives any federal, state or private scholarships. We do not include that aid in our estimate, because it’s money that you can take to any college. In addition, our net price is based on the average student’s time-to-degree. If you finish in four years, that likely will reduce your cost.

Acknowledgements

Former Money senior writer Kim Clark was instrumental in developing our methodology and rankings. Money is thankful to several higher education experts whose insights every year help us make decisions on what data to use and how to weigh it.

The Money editorial staff is solely responsible for the final ranking decisions.

Disclaimer: All the information for Money’s Best Colleges of 2025, which includes tuition prices, financial aid, percentages, average student debt and early career earnings, was researched by Money. However, Money does not guarantee that this information will apply to each person nor guarantees any early career earnings.